Poor bookkeeping is one of the most common reasons small businesses in the LS25 area face unexpected tax bills, HMRC enquiries, or simply run out of cash at the worst possible moment. A missed receipt here, a forgotten invoice there, and suddenly your year-end accounts are a mess. The good news is that bookkeeping is essential for financial management and compliance, and with the right process in place, it does not have to be complicated. This guide walks you through every stage, from understanding the basics to reviewing your records with confidence.

Table of Contents

- Understanding the basics of bookkeeping

- What you need before you start: tools and requirements

- Step-by-step: how to prepare your bookkeeping

- Common mistakes and how to avoid them

- Checking your work and preparing for compliance

- Bookkeeping made easy with local experts

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Start with clear records | Collect all necessary documents and choose the right tools before you begin bookkeeping. |

| Follow a structured process | Completing bookkeeping in regular steps helps reduce mistakes and save time. |

| Avoid common pitfalls | Watch out for missing receipts and duplicate entries to prevent compliance problems. |

| Check and plan regularly | Routine reviews of your records make tax preparation and compliance much simpler. |

Understanding the basics of bookkeeping

Bookkeeping is simply the process of recording every financial transaction your business makes. Every sale, every purchase, every bank transfer. Think of it as a running diary of your business's money. Without it, you are essentially flying blind when it comes to tax returns, cash flow decisions, and planning for growth.

At its core, bookkeeping forms the foundation for tax compliance and business growth. HMRC requires accurate records to verify your tax returns, and your own management decisions depend on knowing exactly where money is coming from and going to. If you are also handling bookkeeping for self assessment, accurate records become even more critical.

Here are the key terms every LS25 business owner should know:

- Invoice: A document you send to customers requesting payment for goods or services.

- Receipt: Proof that a payment has been made, either by you or to you.

- Ledger: A record that groups all transactions by category, such as sales or expenses.

- Accounts: Summaries of your financial position, often broken into income, expenses, assets and liabilities.

"Many small businesses in LS25 overlook petty cash transactions and small supplier invoices. These small amounts add up quickly and can cause real headaches at year-end if they are not recorded consistently."

What you need before you start: tools and requirements

Before you enter a single transaction, gather everything you need. Proper preparation shortens bookkeeping time and reduces errors significantly. Jumping in without the right documents is like trying to bake without checking you have all the ingredients first.

Here is a quick overview of what you will need:

| Item | Why you need it | Where to find it |

|---|---|---|

| Bank statements | Verify all income and outgoings | Online banking or paper statements |

| Sales invoices | Record all money owed to you | Your invoicing system or email |

| Purchase receipts | Claim allowable expenses | Paper, email, or receipt apps |

| Payroll records | Report staff costs accurately | Payroll software or your accountant |

| VAT records | Complete VAT returns correctly | Accounting software or spreadsheets |

Every business should also keep the following for HMRC purposes:

- All sales and income records

- All business expenses and purchase receipts

- Bank and credit card statements

- VAT records if you are VAT registered

- Payroll records if you employ staff

- Records of any assets purchased for the business

When it comes to choosing your method, you have three main options: paper records, spreadsheets, or dedicated accounting software. Paper works for very simple sole traders but becomes unwieldy fast. Spreadsheets offer more flexibility and are free, but they require discipline. Accounting software automates much of the process and reduces human error. Use this UK accounting checklist to make sure you have covered every requirement before you begin.

Pro Tip: Set up a dedicated folder on your computer or cloud storage for each tax year. Label subfolders by month and category. Doing this from day one saves hours of frantic searching come January.

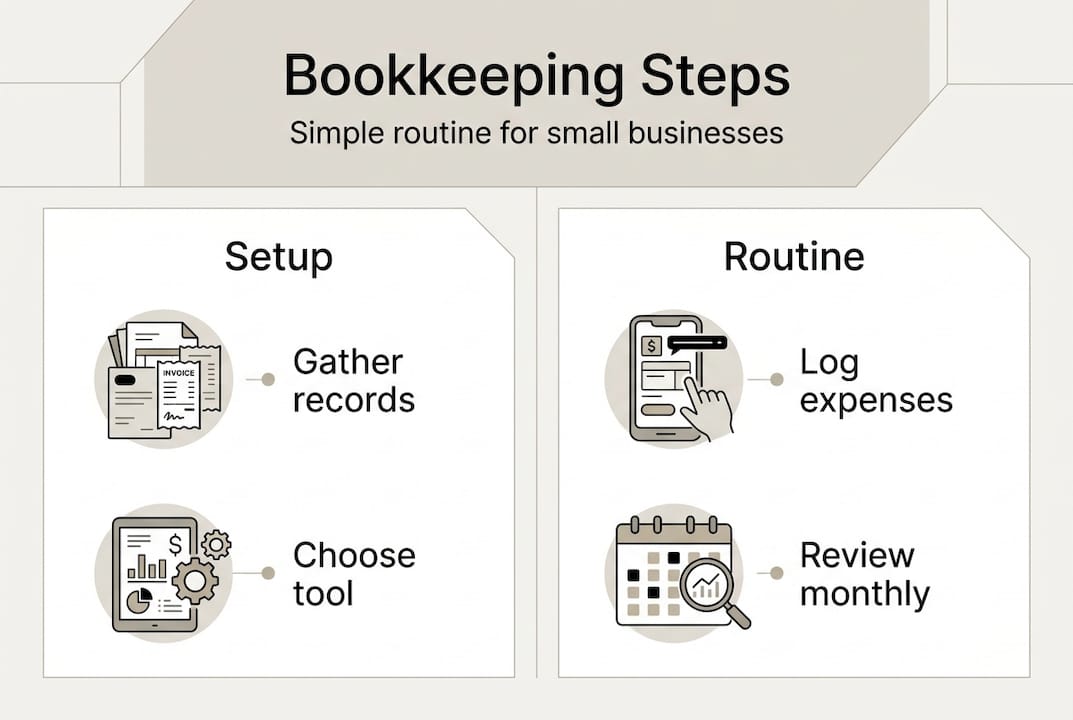

Step-by-step: how to prepare your bookkeeping

Once you have everything ready, here is how to actually start. Following a structured process helps small businesses avoid costly errors that are difficult to unpick later.

- Gather all your records. Collect every invoice, receipt, bank statement and payroll document for the period you are working on. Do not skip anything, even small amounts.

- Choose your bookkeeping method. Decide whether you will use paper, a spreadsheet, or accounting software. The right bookkeeping method can optimise efficiency and accuracy for your specific business size and type.

- Enter all transactions. Record every income and expense in your chosen system. Match each entry to a supporting document such as an invoice or receipt.

- Reconcile your bank account. Compare your records against your bank statements line by line. Any discrepancy needs investigating before you move on.

- Review and categorise. Make sure every transaction is assigned to the correct category, such as office supplies, travel, or sales income. Correct categorisation directly affects your tax return.

- File your supporting documents. Store all receipts and invoices in an organised way, either physically or digitally, so you can retrieve them quickly if HMRC asks.

Here is a comparison to help you choose the right approach:

| Method | Best for | Cost | Effort required |

|---|---|---|---|

| Paper records | Very small sole traders | Free | High |

| Spreadsheets | Small businesses, basic needs | Free | Medium |

| Accounting software | Growing businesses, VAT registered | Monthly fee | Low |

Pro Tip: Batch similar tasks together. Set aside 30 minutes every Friday to enter that week's expenses. It takes far less time than trying to reconstruct three months of records in one sitting.

Common mistakes and how to avoid them

Even a good system fails if mistakes creep in. Here are the errors that catch LS25 business owners out most often:

- Misplacing receipts. A missing receipt means you cannot claim that expense. Use a receipt scanning app on your phone to capture them immediately.

- Duplicate entries. Entering the same transaction twice inflates your expenses or income and distorts your accounts. Always reconcile against your bank statement.

- Mixing personal and business finances. This is one of the most damaging habits. Open a dedicated business bank account and never use it for personal spending.

- Ignoring small transactions. Cash purchases under a few pounds are easy to forget, but they accumulate and create gaps in your records.

- Leaving it all to year-end. Trying to reconstruct 12 months of records in one go is stressful, error-prone, and time-consuming.

Simple errors in record-keeping can lead to HMRC fines and missed savings. A single VAT filing error, for example, can trigger a penalty even if it was accidental. Read our VAT filing errors guide for specific pitfalls to avoid, and our guide on managing business expenses for practical tips on keeping costs organised.

"A sole trader in the LS25 area once faced a £1,200 HMRC penalty because three years of expense receipts had been stored in a carrier bag and many were illegible. The records could not support the deductions claimed, and HMRC disallowed them entirely."

Set diary reminders every week to update your records. Consistency is the single biggest factor in keeping your bookkeeping accurate.

Checking your work and preparing for compliance

After putting everything in place, one final step remains: reviewing your records to make sure they are solid and ready for scrutiny. Regular reviews reduce errors and make compliance straightforward, rather than a last-minute scramble.

Work through this checklist before any tax deadline:

- Confirm every bank transaction has a matching record in your books.

- Check that all invoices issued have been marked as paid or outstanding.

- Verify that all expense receipts are filed and match the entries in your accounts.

- Review your VAT records if applicable and ensure they match your returns.

- Check payroll records are complete and match payments made to staff.

- Confirm that personal and business transactions have not been mixed.

- Run a profit and loss summary to sense-check your figures against your expectations.

Use your tax planning checklist to align your bookkeeping review with upcoming deadlines. Understanding the benefits of tax planning also helps you see how well-kept records translate directly into legitimate tax savings.

Pro Tip: Set up automated monthly reports in your accounting software. A quick glance at your profit and loss each month takes five minutes and flags problems before they become serious.

Regular checks also support better business decisions. When your records are current and accurate, you can see exactly how your business is performing, spot trends early, and plan with confidence rather than guesswork.

Bookkeeping made easy with local experts

If working through all of this feels like a lot to manage alongside running your business, you are not alone. Many LS25 sole traders and small business owners find that setting up a reliable bookkeeping system is the hardest part, especially when compliance requirements keep changing.

LS25 Accountants offers tailored support for exactly the challenges covered in this guide, from setting up your first bookkeeping system to reviewing records before a tax deadline. Whether you want a one-off health check or ongoing support, the team understands the specific needs of businesses in the LS25 area. Book a free consultation to get your records in order and take the stress out of compliance for good.

Frequently asked questions

What records do I need to keep for HMRC?

You must keep full records including invoices, bank statements, expense receipts and all business transaction records for at least six years.

Can I do my own bookkeeping or should I use an accountant?

Small businesses can manage their own simple bookkeeping, but expert support keeps business records compliant and accurate as your business grows and transactions become more complex.

What is the best bookkeeping method for a sole trader?

Many sole traders use spreadsheets or simple accounting apps, and selecting the right method makes the process easier and less time-consuming from the outset.

How often should I update my bookkeeping records?

Consistent record-keeping reduces errors and eases compliance, so aim to update records weekly at a minimum, with daily updates being ideal for busier businesses.