Running a limited company means wearing many hats, and tax is one of the trickiest. Many directors assume their company tax return and their personal Self Assessment are the same thing. They are not. As both returns may be needed, confusing the two can lead to missed deadlines, unexpected penalties, and a very unwelcome letter from HMRC. This guide cuts through the confusion, explains exactly what your company must file, and shows you how to keep more of your profits legally and efficiently.

Table of Contents

- What is a limited company tax return?

- Key corporation tax deadlines and penalties

- Understanding corporation tax rates and thresholds

- How to complete your CT600 and supporting documents

- Optimising taxable profits and claims

- Edge cases and special situations

- Essential tips for staying compliant and digital

- Expert support for your company tax returns

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Filing is not optional | Every limited company must file a CT600 return every year, even if no profit is made or the company is dormant. |

| Know your deadlines | You must pay tax within 9 months and 1 day and file your return by 12 months after your accounting period ends. |

| Use all available reliefs | Claim every legitimate deduction and relief, such as capital allowances, to minimise your corporation tax bill. |

| Digital compliance is growing | From April 2026, commercial software will be required for online filing and digital records will be the norm. |

| Penalties can add up fast | Even a single missed deadline can quickly lead to hundreds of pounds in penalties and interest. |

What is a limited company tax return?

A limited company tax return is not the same as a personal tax return. It is a formal submission to HMRC that reports your company's financial activity for a given accounting period. The form at the centre of this process is the CT600.

The CT600 requires company details, turnover, trading profits and losses, chargeable gains, deductions and reliefs such as capital allowances, and a full tax calculation. It must be submitted alongside iXBRL-tagged accounts and tax computations. iXBRL stands for Inline eXtensible Business Reporting Language, which is simply a digital format that allows HMRC to read your accounts electronically.

This is very different from a personal Self Assessment return, which covers your income as an individual, including any salary or dividends you draw from the company. Both may be required if you are a director taking income from your company.

Getting business tax compliance right from the start protects you from penalties and keeps your company's financial records clean and audit-ready.

Key items required in a CT600:

- Company registration number and accounting period dates

- Turnover and trading profit or loss figures

- Chargeable gains from asset disposals

- Capital allowances and other deductions

- R&D relief claims where applicable

- Final corporation tax calculation

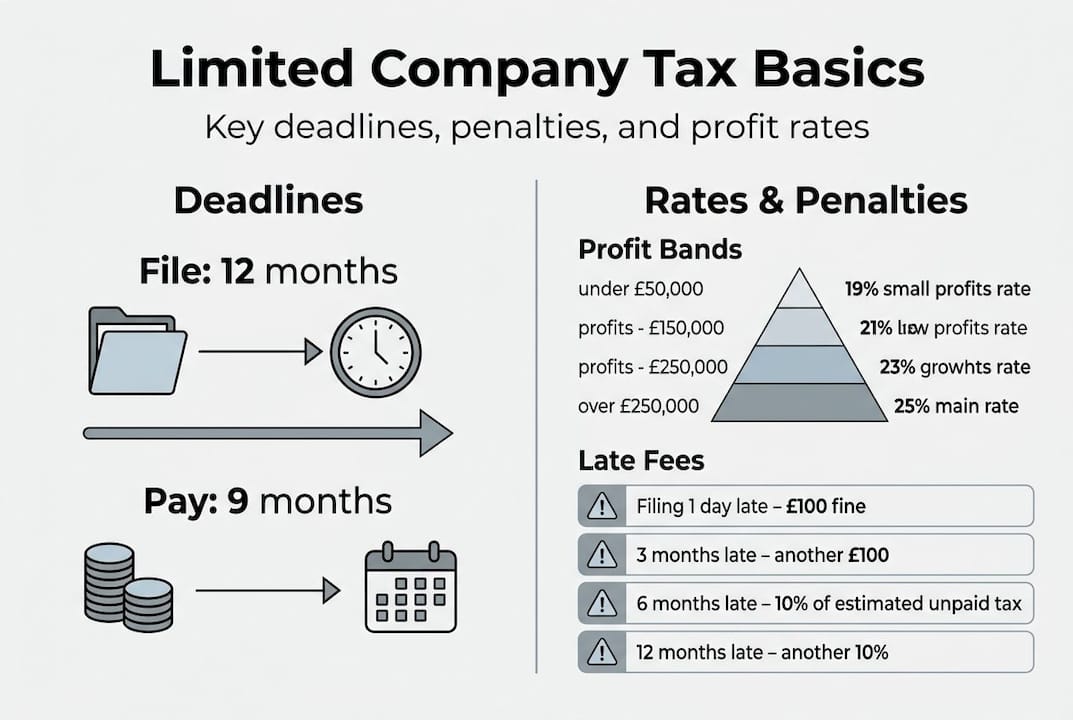

Key corporation tax deadlines and penalties

Staying compliant with HMRC's deadlines is non-negotiable. Miss them and the costs add up fast.

The filing deadline is 12 months after the end of your accounting period. However, your payment deadline is earlier: 9 months and 1 day after the accounting period ends. Many directors get caught out by this distinction.

| Event | Deadline |

|---|---|

| Corporation tax payment due | 9 months and 1 day after period end |

| CT600 filing deadline | 12 months after period end |

| Penalty for 1 day late | £100 |

| Penalty at 3 months late | Additional £100 |

| Penalty at 12 months late | Up to £200 plus 20% of tax |

From April 2026, late filing penalties increase to £200 for the initial penalty and £400 at three months. Interest on late payments currently runs at 7.75% or above from the due date.

Important: The payment deadline comes before the filing deadline. Many directors assume they have 12 months to pay. They do not.

Pro Tip: Set a calendar reminder for both deadlines the moment your accounting period closes. Pair this with accounting tips for tax deadlines to build a reliable annual routine.

Understanding corporation tax rates and thresholds

Knowing what you owe and why is just as important as filing on time.

Corporation tax rates currently sit at 19% on profits up to £50,000 and 25% on profits above £250,000. For profits between £50,001 and £250,000, marginal relief applies, meaning your effective rate rises gradually rather than jumping sharply to 25%.

| Profit band | Rate |

|---|---|

| Up to £50,000 | 19% (small profits rate) |

| £50,001 to £250,000 | Marginal relief applies |

| Over £250,000 | 25% (main rate) |

The marginal relief fraction of 3/200 prevents a cliff-edge jump in tax. In practice, the effective marginal rate within that band can reach 26.5%, so it pays to model your tax position carefully as profits approach £250,000.

One often-overlooked rule involves associated companies. If your company has associated companies (broadly, companies under common control), the thresholds are divided between them. Two associated companies each get a £25,000 small profits threshold, not £50,000.

For context, recent corporation tax statistics show that the vast majority of UK companies report profits well below £50,000, meaning most pay the 19% small profits rate.

Pro Tip: Review your UK tax thresholds 2026 position before your year end. If profits are just above £50,000, a pension contribution or capital investment could bring you back into the lower rate band.

How to complete your CT600 and supporting documents

Now you know how much tax you owe, here is exactly what you need to file and how to go about it.

The CT600 filing process involves preparing your accounts, tagging them in iXBRL format, completing the CT600 form itself, and submitting everything to HMRC online. From April 2026, HMRC's free filing service ends, so you will need commercial software.

Step-by-step CT600 filing process:

- Finalise your company accounts for the accounting period

- Prepare your tax computation, adjusting accounting profit for disallowable items

- Tag your accounts in iXBRL format using compatible software

- Complete the CT600 form with all required figures

- Claim all available reliefs, including full expensing for 100% capital allowances on qualifying plant and machinery

- Submit the CT600 and iXBRL accounts to HMRC before the 12-month deadline

- Pay any tax owed before the 9-month-and-1-day deadline

Pro Tip: Use accounting software tips to choose software that handles iXBRL tagging automatically. This removes one of the most error-prone steps in the process.

Optimising taxable profits and claims

Filling out the forms is one thing. Smart companies make sure they do not pay a penny more than necessary.

Your taxable profit is your accounting profit adjusted for disallowable expenses, then reduced by allowances and reliefs. Disallowable expenses are costs that appear in your accounts but cannot be deducted for tax purposes. Client entertaining is a classic example.

Common reliefs and deductions to claim:

- Capital allowances on equipment, vehicles, and fixtures

- Full expensing (100% first-year allowance on qualifying assets)

- R&D tax relief for qualifying innovation activities

- Director salary and employer pension contributions

- Losses carried forward from previous periods

Timing matters too. If your profits are close to a threshold, deferring income to the next accounting period or accelerating deductible expenses into the current one can shift your tax position meaningfully. This is entirely legal and forms part of sound corporate tax planning strategies.

A well-structured tax planning checklist reviewed before your year end ensures no relief is missed. The corporation tax reliefs available from HMRC cover a wide range of scenarios, and many directors leave money on the table simply by not knowing what they can claim. A thorough tax deduction guide can help you identify every legitimate saving.

Edge cases and special situations

Most companies follow a straightforward annual cycle, but several situations require a different approach.

First-time filers often encounter a common issue: if your first accounting period is longer than 12 months (which happens when a company is incorporated mid-year), you must split it into two separate CT600 returns. Each return covers a distinct period and has its own deadlines.

Situations that require special handling:

- First accounting period over 12 months: Split into two returns, each filed separately

- Short accounting periods: Tax thresholds are prorated to reflect the shorter period

- Dormant companies: A simplified return is still required; you cannot simply ignore the obligation

- Group companies: Use the CT600C supplementary form to report group relief

- Non-UK resident companies: Different filing rules may apply depending on the nature of UK activity

For dormant companies in particular, many directors assume no trading means no filing. That assumption is wrong and can lead to automatic penalties. Solid business tax preparation guidance covers these scenarios in detail.

Essential tips for staying compliant and digital

With the technical details covered, it helps to build ongoing routines that keep your company compliant and efficient.

MTD for corporation tax is not yet mandated, but digital record keeping is already essential. HMRC expects accurate, well-organised records, and digital systems make it far easier to produce the iXBRL accounts required for CT600 filing.

Your annual compliance checklist:

- Keep digital records of all income, expenses, and bank transactions throughout the year

- Reconcile your accounts monthly rather than leaving it all to year end

- Choose software that supports iXBRL tagging and direct HMRC submission

- Note both your payment deadline and filing deadline in your calendar immediately after your period closes

- Review available reliefs and allowances before finalising your tax computation

- File and pay on time to avoid the penalty increases taking effect from April 2026

- Check your VAT compliance guide obligations run alongside your corporation tax duties without overlap or gaps

Building these habits means tax season becomes a routine task rather than a stressful scramble.

Expert support for your company tax returns

Managing corporation tax correctly takes time, knowledge, and attention to detail. Even experienced directors can miss a relief, miscalculate a threshold, or overlook a deadline change. Professional support removes that risk entirely.

At LS25 Accountants, we work with limited company directors across the LS25 area to handle CT600 preparation, iXBRL filing, tax optimisation, and compliance planning. Whether you are filing your first return or managing a growing group structure, our team ensures your company stays on the right side of HMRC while claiming every relief you are entitled to. Get in touch to find out how we can take the complexity out of your company tax obligations.

Frequently asked questions

What is the deadline for filing a limited company tax return in the UK?

The filing deadline is 12 months after the end of your company's accounting period, but payment is due earlier at 9 months and 1 day after the period ends.

Do I need to file a company tax return if my company made no profit?

Yes. Even dormant companies must file a CT600 return with HMRC, regardless of whether any trading took place during the period.

How do I calculate corporation tax for small companies?

Tax is 19% on profits up to £50,000, with marginal relief gradually increasing the effective rate for profits between £50,001 and £250,000.

What happens if a company tax return is filed late?

Penalties start at £100 from day one and escalate the longer the return remains outstanding, with interest also charged on any unpaid tax from the payment due date.

Is Making Tax Digital (MTD) required for corporation tax yet?

MTD for corporation tax is not mandated before April 2026, but maintaining digital records now puts your company in a strong position for when the requirement does arrive.