Bookkeeping often feels like a tedious chore, yet it's the foundation of accurate Self Assessment tax returns. Recent HMRC research reveals that 36% of Self Assessment returns under-report tax, with self-employed taxpayers accounting for 60% of these errors. Many of these mistakes stem from inadequate record-keeping rather than deliberate evasion. For small business owners and self-employed individuals across the UK, mastering bookkeeping isn't just about compliance, it's about protecting your business from penalties whilst maximising legitimate tax savings. This guide explains how effective bookkeeping supports accurate Self Assessment, helps you claim every allowable expense, and keeps you on the right side of HMRC regulations.

Table of Contents

- Key takeaways

- Why is bookkeeping essential for self assessment?

- Common pitfalls of poor bookkeeping and their impact

- How to maintain effective bookkeeping for self assessment success

- Bookkeeping methods compared: cash basis vs traditional accounting

- Explore expert accountancy support for your self assessment

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Accurate records | Without systematic records you are effectively guessing your taxable income, creating serious compliance risks. |

| Record retention five years | HMRC requires keeping invoices, receipts and bank statements for at least five years after the 31 January submission deadline. |

| Claim allowable expenses | Proper record keeping enables you to claim all legitimate business expenses, reducing your tax liability. |

| Digital tools and reconciliations | Using digital bookkeeping tools and regular reconciliations helps minimise errors and lowers audit risk. |

Why is bookkeeping essential for self assessment?

Bookkeeping provides the accurate profit figures you need to complete your Self Assessment tax return correctly. Without systematic records, you're essentially guessing at your taxable income, which creates serious compliance risks. HMRC requires retention of financial records including invoices, receipts, and bank statements for at least 5 years after the 31 January submission deadline. This isn't a suggestion; it's a legal obligation that applies to every self-employed person and small business owner.

The consequences of inadequate records extend beyond inconvenience. HMRC can impose fines up to £3,000 for failing to maintain proper books, and poor documentation makes tax inspections far more complicated and stressful. When inspectors can't verify your figures, they may estimate your income upwards, leaving you with an inflated tax bill you can't effectively challenge. Proper bookkeeping also supports your ability to claim all allowable expenses, directly reducing your tax liability. Without detailed records, you'll miss legitimate deductions simply because you can't prove the expenditure.

Key documents you must retain include:

- Sales invoices and records of all income received

- Purchase invoices and receipts for business expenses

- Bank and credit card statements showing business transactions

- Mileage logs with dates, distances, and business purposes

- Payroll records if you employ staff

- VAT records if you're registered

"Maintaining complete and accurate records isn't just about avoiding penalties. It's about having a clear picture of your business finances so you can make informed decisions and plan effectively for tax obligations."

Understanding tax compliance requirements helps you appreciate why bookkeeping sits at the heart of successful Self Assessment. The effort you invest in maintaining good records pays dividends when tax season arrives, transforming what could be a stressful scramble into a straightforward process.

Common pitfalls of poor bookkeeping and their impact

Many small business owners lack systematic bookkeeping processes, creating a cascade of errors that affect reported income and expenses. The statistics are sobering: research shows that 60% of under-reporting comes from self-employed taxpayers, with a small minority of careless record-keepers causing nearly half the tax gap. These aren't necessarily dishonest people; they're busy entrepreneurs who underestimate how quickly poor bookkeeping habits compound into serious problems.

Typical pitfalls include missing receipts that prevent you from claiming legitimate expenses, mixing personal and business expenditure in the same accounts, and updating records sporadically rather than regularly. Each mistake seems minor in isolation, but together they create an inaccurate financial picture. When you finally sit down to complete your Self Assessment, you're forced to estimate figures you should know precisely, increasing the likelihood of errors that trigger HMRC scrutiny.

Under-reporting risks have real consequences:

- HMRC audits that require extensive documentation you may not have

- Recovery of unpaid tax plus interest charges

- Penalties ranging from 15% to 100% of the unpaid tax depending on circumstances

- Reputational damage if serious errors are publicised

- Increased likelihood of future inspections once you're flagged

Consider practical examples of how poor bookkeeping costs you money. Missing expense claims means you pay tax on profits that don't reflect your true costs, artificially inflating your tax bill. Failing to record cash income creates unrecorded transactions that, if discovered, look like deliberate evasion even when they're simple oversights. Losing receipts for major purchases means you can't claim capital allowances, missing out on significant tax relief.

"The difference between a tax investigation that's quickly resolved and one that drags on for months often comes down to the quality of your bookkeeping. Good records provide clear evidence that supports your position."

Understanding what triggers tax audits helps you appreciate why maintaining accurate books isn't paranoia, it's practical risk management. The time you save by cutting corners on bookkeeping rarely compensates for the stress and cost when problems emerge.

How to maintain effective bookkeeping for self assessment success

Adopting digital bookkeeping software that automatically imports bank feeds transforms your record-keeping accuracy. Manual data entry creates opportunities for typos and omissions, whilst automated systems capture every transaction in real time. Modern cloud-based platforms categorise expenses intelligently, flag unusual transactions, and generate reports instantly, giving you a current view of your financial position without hours of manual work.

Follow these monthly reconciliation steps to maintain accuracy:

- Download your bank and credit card statements at month end

- Compare every transaction against your bookkeeping records

- Investigate and resolve any discrepancies immediately

- Review expense categories to ensure correct classification

- Check that all income has been properly recorded

- Generate a profit and loss statement to monitor performance

Retaining documents securely for at least 5 years after your Self Assessment deadline protects you during potential inspections. Digital storage offers advantages over paper: it's searchable, backed up automatically, and doesn't require physical space. Scan receipts immediately using your phone, tagging them with relevant transaction details so you can find them instantly when needed. Cloud storage with encryption ensures your sensitive financial data remains secure whilst accessible from anywhere.

Record expenses promptly with clear categorisation to claim all allowable deductions. Waiting until year end to sort through a shoebox of receipts guarantees you'll miss items and struggle to remember what purchases were for. Instead, photograph receipts as you receive them, noting the business purpose whilst it's fresh in your mind. This habit takes seconds per transaction but saves hours during tax preparation.

Pro Tip: Keep a mileage log in your vehicle with columns for date, starting location, destination, business purpose, and miles travelled. HMRC's approved mileage rates provide generous tax relief, but only if you can demonstrate the business nature of each journey with contemporaneous records.

| Bookkeeping task | Frequency | Time required | Impact on accuracy |

|---|---|---|---|

| Record transactions | Daily | 5-10 minutes | High - prevents backlog |

| Reconcile accounts | Monthly | 30-60 minutes | Critical - catches errors early |

| Review categories | Monthly | 15-20 minutes | Medium - ensures correct reporting |

| Back up records | Weekly | 5 minutes | High - protects against data loss |

| Generate reports | Quarterly | 20-30 minutes | Medium - monitors business health |

Effective cash flow management depends on accurate bookkeeping that shows you exactly where money enters and leaves your business. When you know your numbers precisely, you can plan tax payments, invest in growth opportunities, and avoid nasty surprises.

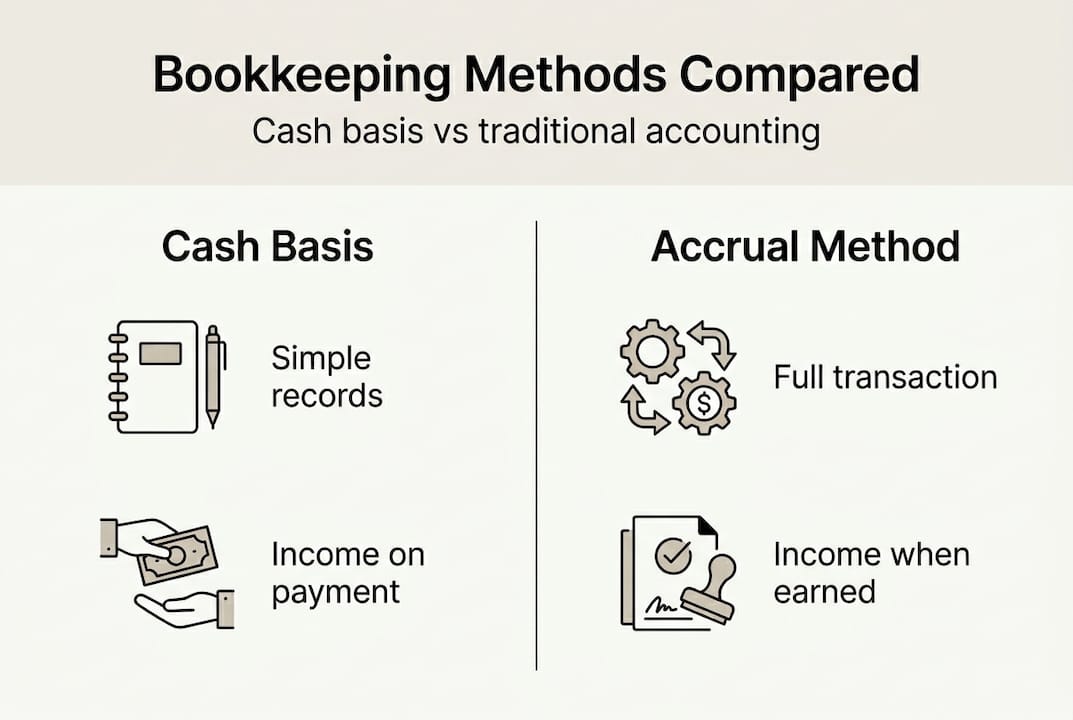

Bookkeeping methods compared: cash basis vs traditional accounting

Cash basis accounting records income when you receive payment and expenses when you pay them, matching your bank account activity. This straightforward approach suits many self-employed individuals because it's intuitive: if money hits your account, it's income; if money leaves, it's an expense. You don't need to track invoices issued but not yet paid, or bills received but not yet settled. For simple businesses with straightforward transactions, cash basis reduces bookkeeping complexity significantly.

Traditional accrual accounting recognises transactions when they're earned or incurred, regardless of payment timing. If you invoice a client in March but receive payment in April, accrual accounting records the income in March. This method provides a more accurate picture of business performance by matching revenue with the expenses incurred to generate it, but requires more detailed record-keeping including tracking receivables and payables.

| Feature | Cash basis | Traditional accrual |

|---|---|---|

| When income recorded | Money received | Invoice issued |

| When expenses recorded | Money paid | Bill received |

| Complexity | Simple, follows bank account | More detailed tracking needed |

| Best for | Small businesses, simple transactions | Larger businesses, complex operations |

| Tax timing | May defer tax if paid slowly | Matches economic activity |

| Financial insight | Cash position clear | Profit picture more accurate |

Cash basis limits certain complex transactions but dramatically reduces bookkeeping time and potential errors. You can't claim losses on bad debts or stock value changes, but for service businesses without inventory, these limitations rarely matter. The simplified approach means fewer opportunities for mistakes, particularly valuable if you're managing books yourself alongside running your business.

Accrual accounting provides better matching of income and expenses, offering clearer insight into whether specific projects or periods were truly profitable. However, it requires tracking additional information: who owes you money, who you owe, and when payments are due. This extra complexity increases the risk of errors if you're not experienced with accounting principles.

Pro Tip: HMRC allows most small businesses with turnover under £150,000 to use cash basis accounting. If you're eligible, seriously consider this option as it simplifies compliance whilst still meeting all legal requirements.

Choosing the right method impacts your tax calculations and financial planning. Cash basis can defer tax if customers pay slowly, since you only report income when received. Accrual accounting may trigger tax on unpaid invoices, requiring careful cash flow management to ensure you have funds available when tax comes due. Understanding these differences helps you select the approach that best fits your business model and administrative capacity.

Exploring accounting methods and tips provides additional context for making informed decisions about your bookkeeping approach, particularly as your business grows and evolves.

Explore expert accountancy support for your self assessment

Managing bookkeeping and Self Assessment becomes increasingly complex as your business grows, consuming valuable time you could spend serving customers or developing new opportunities. Professional accountants provide tailored advice ensuring compliance whilst identifying tax-saving opportunities you might miss. They understand the nuances of allowable expenses, capital allowances, and timing strategies that legally minimise your tax burden.

LS25 Accountants offer expert guidance and practical solutions specifically designed for self-employed clients and small businesses across the LS25 area. Our team stays current with changing tax regulations, ensuring your Self Assessment reflects the latest rules and maximises available reliefs. Using specialised accountancy services helps you avoid costly mistakes whilst freeing you to focus on what you do best: growing your business and serving your clients with confidence.

Frequently asked questions

What is the primary purpose of bookkeeping for self assessment?

Bookkeeping accurately tracks all business income and expenses, providing the precise figures you need to calculate taxable profits for your Self Assessment return. Without systematic records, you cannot determine your true tax liability or prove your figures to HMRC if questioned.

How long must I keep financial records after submitting self assessment?

HMRC requires you to retain all financial records for at least 5 years after the 31 January submission deadline. This includes invoices, receipts, bank statements, and any other documents supporting your tax return figures.

Can digital bookkeeping tools help me stay compliant?

Digital tools dramatically improve compliance by automatically importing bank transactions, categorising expenses intelligently, and flagging unusual items for review. They reduce manual errors, provide real-time financial visibility, and generate reports instantly for Self Assessment preparation.

What penalties apply if I maintain poor records?

HMRC can fine you up to £3,000 for inadequate record-keeping, separate from any penalties for incorrect tax returns. Poor records also increase audit risks and make it difficult to defend your position if HMRC questions your figures.

How does good bookkeeping maximise my expense claims?

Systematic bookkeeping ensures you capture and categorise every allowable business expense with supporting documentation. This means you claim all legitimate deductions rather than missing items due to lost receipts or forgotten transactions, directly reducing your tax bill.