Many UK small business owners and sole traders unknowingly leave thousands of pounds on the table each year by failing to claim legitimate tax allowable expenses. A common misconception is that only major purchases qualify, when in reality everyday business costs from office supplies to mileage can significantly reduce your taxable income. Understanding which expenses HMRC permits and how to claim them correctly transforms your financial efficiency whilst ensuring full compliance. This guide walks you through the essential categories, the strict rules governing claims, and practical strategies to maximise your tax savings without triggering audits or penalties.

Table of Contents

- Key takeaways

- What are tax allowable expenses?

- Common categories of allowable expenses with examples

- Expenses that cannot be claimed and the 'wholly and exclusively' test

- How to maximise your claims using simplified expenses and best practices

- How LS25 Accountants can help your business optimise tax expenses

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Core expense categories | HMRC recognises core expense categories that reduce taxable profit, including office costs, travel, staff costs, marketing, insurance and financial fees. |

| Wholly exclusive rule | Expenses must be incurred wholly and exclusively for the trade, with personal use kept to a minimum. |

| Benefits of simplified expenses | Simplified methods offer predictable amounts and easier claiming for items such as home office and mileage allowances. |

| Dedicated business accounts | Using a dedicated business bank account and credit card helps separate business expenses from personal spending and streamlines year end claims. |

What are tax allowable expenses?

Tax allowable expenses are business costs you can deduct from your revenue before calculating the profit subject to tax. HMRC defines these as expenses incurred 'wholly and exclusively' for your trade or profession, meaning the expenditure must serve a genuine business purpose without significant personal benefit. For sole traders, these deductions reduce profit before Income Tax calculations, whilst limited companies deduct them before Corporation Tax, though the fundamental principles remain consistent across structures. Sole traders deduct before Income Tax; limited companies before Corporation Tax with similar rules but different structures.

The impact on your tax bill can be substantial. If you run a graphic design business as a sole trader earning £45,000 annually and claim £8,000 in allowable expenses, you pay tax only on £37,000 rather than the full amount. This saves you thousands depending on your tax band. Limited companies enjoy similar benefits, with allowable expenses reducing the profit figure subject to the 19% Corporation Tax rate in 2026.

Typical qualifying costs include:

- Office rent, utilities, and equipment necessary for daily operations

- Professional fees for accountants, solicitors, and industry advisors

- Marketing expenditure from website hosting to advertising campaigns

- Staff salaries, employer National Insurance, and pension contributions

- Business insurance policies covering liability, property, and professional indemnity

- Travel costs directly related to business activities excluding normal commuting

Understanding these fundamentals helps you recognise opportunities throughout the year rather than scrambling at tax return deadlines. Implementing proper tax planning benefits for small businesses by building expense tracking into your routine financial management. The key distinction between allowable and non-allowable expenses lies in that strict 'wholly and exclusively' criterion, which we explore in detail later.

Pro tip: Set up a dedicated business bank account and credit card to automatically separate business expenses from personal spending, making year-end claims far simpler and audit-proof.

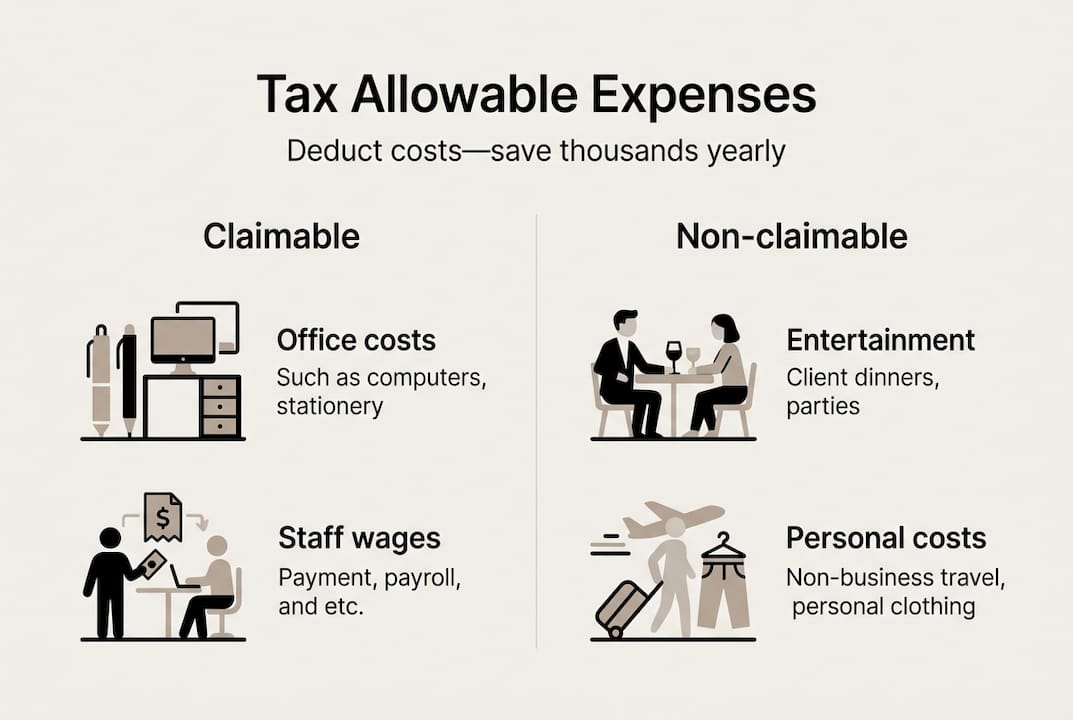

Common categories of allowable expenses with examples

HMRC recognises several core expense categories that apply across most UK small businesses and sole traders. Key categories include office costs, travel, staff, marketing, insurance, financial fees, and simplified expenses for home office. Understanding each category with concrete examples helps you identify claims you might otherwise miss.

Office and premises costs cover rent, business rates, utilities, and maintenance for dedicated business spaces. If you rent a shop or office, the full amount qualifies. Home workers can claim a proportion of household bills based on business use, or opt for simplified expenses of £10 monthly for 25-50 hours, £18 for 51-100 hours, or £26 for 101+ hours.

Travel and vehicle expenses include business mileage, public transport, parking, and accommodation when travelling for work purposes. The simplified mileage rate stands at 45p per mile for the first 10,000 miles annually, then 25p thereafter. Alternatively, claim actual vehicle costs like fuel, insurance, repairs, and depreciation apportioned by business use percentage. Keep detailed mileage logs noting date, destination, purpose, and miles travelled.

Staff costs encompass salaries, wages, bonuses, employer National Insurance contributions, pension payments, and employee benefits like training courses. Subcontractor fees also qualify when you hire freelancers or agencies. Recruitment expenses including job advertising and agency fees are fully allowable.

Marketing and advertising covers website development and hosting, social media advertising, printed materials, promotional events, and sponsorships that generate business exposure. Professional photography for marketing materials, SEO services, and email marketing platforms all qualify under this umbrella.

Insurance and financial costs include professional indemnity, public liability, business property insurance, accountancy fees, bank charges, and interest on business loans. Legal fees for business contracts, debt recovery, and employment matters are allowable, though personal legal issues are not.

| Category | Example expenses | Typical annual range |

|---|---|---|

| Office costs | Rent, utilities, equipment, stationery | £2,000-£15,000 |

| Travel | Mileage, train fares, accommodation | £1,500-£8,000 |

| Staff costs | Salaries, NI, pensions, training | £15,000-£150,000 |

| Marketing | Website, advertising, materials | £1,000-£10,000 |

| Insurance | Liability, property, professional | £500-£3,000 |

| Financial | Accountant, bank charges, loan interest | £800-£5,000 |

The simplified expenses scheme offers an alternative calculation method for home office and vehicle costs, reducing administrative burden whilst often delivering comparable tax relief. You can mix methods, using simplified for one category and actual costs for another, choosing whichever produces the higher claim. Review your circumstances annually as business patterns change.

Pro tip: Photograph receipts immediately using a cloud storage app to create automatic backups, preventing lost claims when paper receipts fade or go missing before year end. For comprehensive guidance on maximising deductions, explore our tax deduction guide 2026.

Expenses that cannot be claimed and the 'wholly and exclusively' test

HMRC maintains strict boundaries around what qualifies as allowable, with non-allowable expenses including client entertainment, normal clothing, fines, commuting, personal food. Understanding these exclusions prevents costly errors that trigger audits and penalties whilst ensuring your legitimate claims withstand scrutiny.

The legal foundation rests on the 'wholly and exclusively' principle established through decades of tax case law. This means the expense must serve business purposes alone, with no significant personal benefit. The HMRC 'wholly & exclusively' test is strict: incidental personal benefit disallows the claim as demonstrated in the landmark Mallalieu v Drummond case where a barrister could not claim clothing costs despite wearing outfits only for court appearances.

Common disallowed expenses include:

- Client entertainment such as meals, drinks, tickets, or hospitality events regardless of business discussion occurring

- Normal commuting between home and your regular workplace, though travel between business sites qualifies

- Everyday clothing even if worn exclusively for work, unless it is specialist protective equipment or branded uniforms

- Personal food and drink except when travelling overnight on business or working unusually late hours

- Fines, penalties, and parking tickets which HMRC views as punitive rather than business costs

- Gym memberships and health costs unless demonstrably required for your specific trade

- Personal phone and internet costs, though business use portions of bills qualify

The dual-purpose trap catches many businesses. If an expense serves both business and personal purposes, you must apportion it accurately or risk losing the entire claim. A laptop used 70% for business and 30% personally allows you to claim 70% of the cost, but claiming 100% invites challenge. HMRC increasingly uses data analytics to flag disproportionate claims against industry benchmarks.

"The 'wholly and exclusively' test remains one of HMRC's most powerful compliance tools. Even minor personal benefit can disqualify an otherwise legitimate business expense, making accurate record keeping and honest apportionment essential for every claim."

Audit triggers include round numbers suggesting estimates rather than actual receipts, claims significantly above sector averages, and patterns indicating personal expenditure misclassified as business costs. The penalties for deliberate misrepresentation range from 30% to 100% of tax underpaid plus interest, whilst innocent errors typically incur smaller penalties if corrected promptly.

Pro tip: When an expense has any personal element, document your apportionment methodology in writing at the time of purchase, creating contemporaneous evidence that demonstrates reasonable business judgement rather than retrospective justification. Our tax planning checklist 2026 helps you establish compliant systems, whilst our HMRC tax audit guide 2026 prepares you for scrutiny.

How to maximise your claims using simplified expenses and best practices

Maximising allowable expense claims requires systematic tracking, strategic choices between calculation methods, and awareness of commonly missed opportunities. The simplified expenses method uses flat rates to avoid apportionment whilst actual costs can be claimed if higher, giving you flexibility to optimise your position.

Simplified expenses apply primarily to vehicle costs and home office use. For vehicles, you claim 45p per mile for the first 10,000 business miles annually, then 25p per mile thereafter, covering fuel, insurance, repairs, and depreciation in one calculation. Alternatively, track actual vehicle expenses and claim the business use percentage. Compare both methods each year as the optimal choice shifts with mileage patterns and vehicle costs.

Home office simplified expenses use monthly flat rates: £10 for 25-50 hours, £18 for 51-100 hours, £26 for 101+ hours of home working. This covers heating, electricity, internet, and council tax proportions without complex calculations. If your actual apportioned household costs exceed these rates, claim actual expenses instead by calculating the business use percentage of your home.

Follow these steps to maximise claims systematically:

- Implement digital receipt capture immediately after each purchase using smartphone apps that sync to cloud accounting software, eliminating lost documentation.

- Review bank and credit card statements monthly to identify business expenses you might otherwise forget, from subscriptions to professional memberships.

- Calculate both simplified and actual expense methods for vehicles and home office annually, selecting whichever produces the higher deduction.

- Claim capital allowances on equipment purchases over £1,000 using the Annual Investment Allowance, currently £1 million, to deduct the full cost in year one.

- Track small recurring expenses like postage, stationery, software subscriptions, and professional journals that individually seem minor but accumulate substantially.

- Separate mixed-purpose expenses accurately, claiming only the business portion of phone bills, internet, and shared equipment.

Research shows maximising via simplified flat rates if beneficial helps avoid underclaiming, a common costly error. Many businesses fail to claim legitimate expenses simply through poor record keeping or unfamiliarity with allowable categories. Professional development costs including courses, books, and conference attendance qualify when they maintain or improve skills for your current business, not when retraining for a different field.

Pro tip: Schedule a quarterly expense review session to categorise receipts, update mileage logs, and identify any missing documentation whilst memories remain fresh, rather than facing a chaotic scramble at year end when details have faded. Our small business accounting tips 2026 guide provides comprehensive systems for maintaining compliant records throughout the year.

How LS25 Accountants can help your business optimise tax expenses

Navigating tax allowable expenses whilst running your business demands time and expertise many small business owners simply cannot spare. LS25 Accountants specialises in helping UK sole traders and small companies across the LS25 postcode area maximise legitimate expense claims whilst maintaining full HMRC compliance. Our tailored accounting services go beyond basic bookkeeping to provide strategic tax planning that identifies overlooked deductions and optimises your calculation methods.

Our experienced advisors understand the nuances of simplified versus actual expense calculations, helping you choose the most beneficial approach for your specific circumstances. We implement cloud accounting systems that automatically categorise transactions, flag potential claims, and maintain audit-ready documentation. From mileage tracking to home office apportionment, we ensure you claim every pound you are entitled to without crossing compliance boundaries. Explore our comprehensive resources at LS25 Accountants expert guides or review our tax planning checklist 2026 to see how professional support transforms your tax efficiency. Discover more about the value of expert guidance in our article on hiring a tax advisor.

Frequently asked questions

What expenses can a small business claim as allowable?

Allowable expenses include office costs like rent and utilities, travel expenses for business trips, staff wages and National Insurance, marketing expenditure, insurance premiums, and professional fees for accountants or solicitors. These costs must be incurred wholly and exclusively for business purposes to qualify. Simplified flat rates apply for some expenses such as home working and mileage, offering an alternative to tracking actual costs.

What expenses cannot be claimed for UK business tax?

Disallowed expenses include client entertainment regardless of business discussion, commuting costs between home and your regular workplace, fines and parking penalties, dual-purpose clothing worn for work, and personal food unless on overnight business travel. Such costs fail HMRC's 'wholly and exclusively' rule because they provide personal benefit or are punitive in nature. Claiming these expenses risks penalties and audit scrutiny, so accurate categorisation is essential. Review our tax deduction guide 2026 for comprehensive compliance guidance.

How does the simplified expenses scheme work?

Simplified expenses use fixed flat rates for home office and mileage to streamline claims without complex calculations. For home working, you claim £10 to £26 monthly depending on hours worked, covering utility and internet costs proportionally. Vehicle expenses use 45p per mile for the first 10,000 business miles, then 25p thereafter, eliminating the need to track fuel receipts and maintenance costs. You can alternatively claim actual expenses if they are higher, giving you flexibility to maximise your deduction. Compare both methods annually as your optimal choice may change. Our accounting tips 2026 guide explains how to implement efficient tracking systems.

Can a sole trader claim expenses for home working?

Yes, sole traders can claim home working expenses using simplified expenses at £10 monthly for 25 to 50 hours, £18 for 51 to 100 hours, or £26 for 101 plus hours of business use. Alternatively, calculate actual costs by apportioning household bills like heating, electricity, internet, and council tax based on the business use percentage of your home. Choosing the higher method between simplified and actual costs maximises your tax savings. Keep records of hours worked or room usage to support your claim during any HMRC enquiry.