Nearly half of new business owners misunderstand their tax obligations, leading to missed deductions and compliance errors that cost thousands annually. This guide clarifies allowable expenses, Making Tax Digital updates, and capital allowance changes for 2026, helping you reduce your tax bill whilst staying compliant. You'll learn practical strategies to maximise deductions, navigate quarterly reporting requirements, and avoid penalties through proper record keeping and timely submissions.

Table of Contents

- Understanding Allowable Expenses And Their Impact On Your Taxable Profit

- Navigating Making Tax Digital For Income Tax In 2026

- Updates To Capital Allowances: Writing-Down Allowance And First-Year Allowance

- Keeping Accurate Records And Spreading Tax Administration Throughout The Year

- Expert Accountancy Support To Maximise Your 2026 Tax Savings

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Allowable expenses reduce taxable profit | Office costs, travel, marketing, and insurance directly lower your tax bill when claimed correctly. |

| Making Tax Digital starts April 2026 | Sole traders earning over £50,000 must submit quarterly digital updates instead of annual returns. |

| Capital allowances rates changed | Writing-down allowance drops from 18% to 14%, whilst a new 40% first-year allowance encourages equipment investment. |

| Record keeping is essential | Accurate digital records support expense claims and prevent HMRC penalties under new quarterly reporting rules. |

| Grace period for MTD penalties | No penalty points apply for late quarterly updates during your first 12 months under Making Tax Digital. |

Understanding allowable expenses and their impact on your taxable profit

Allowable expenses are costs you can deduct from your business income to reduce your taxable profit. These include office supplies, business travel, marketing expenses, professional insurance, and equipment necessary for daily operations. When you earn £25,000 and claim £5,000 in allowable expenses, you only pay tax on £20,000.

The distinction between allowable and non-allowable expenses determines whether HMRC accepts your claims. Allowable expenses must be incurred wholly and exclusively for business purposes. Personal costs, business entertainment, and client gifts over £50 cannot be claimed. Mixing personal and business expenses without proper allocation triggers HMRC scrutiny and potential penalties.

Self-employed expenses guidance provides clear rules for accurate tax return completion and avoiding penalties. Regular checking of HMRC's list keeps you updated on any changes to allowable categories. Documentation proves every expense claim, so keep receipts, invoices, and bank statements organised digitally.

Common allowable expenses include:

- Office rent, utilities, and equipment for business premises

- Business travel costs including mileage, public transport, and accommodation

- Marketing and advertising expenses for promoting your services

- Professional fees for accountants, solicitors, and industry memberships

- Insurance policies protecting your business and professional liability

- Staff costs including salaries, pensions, and training

Pro Tip: Calculate your home office expenses using HMRC's simplified expenses method at £4 per week for 25-50 hours monthly, saving time on complicated proportional calculations whilst remaining compliant.

Proper expense categorisation connects directly to your tax planning checklist uk business owners 2026 strategy. Understanding allowable expenses guidelines ensures you claim every legitimate deduction. Cross-reference your expense categories with uk tax codes and vat explained for complete compliance.

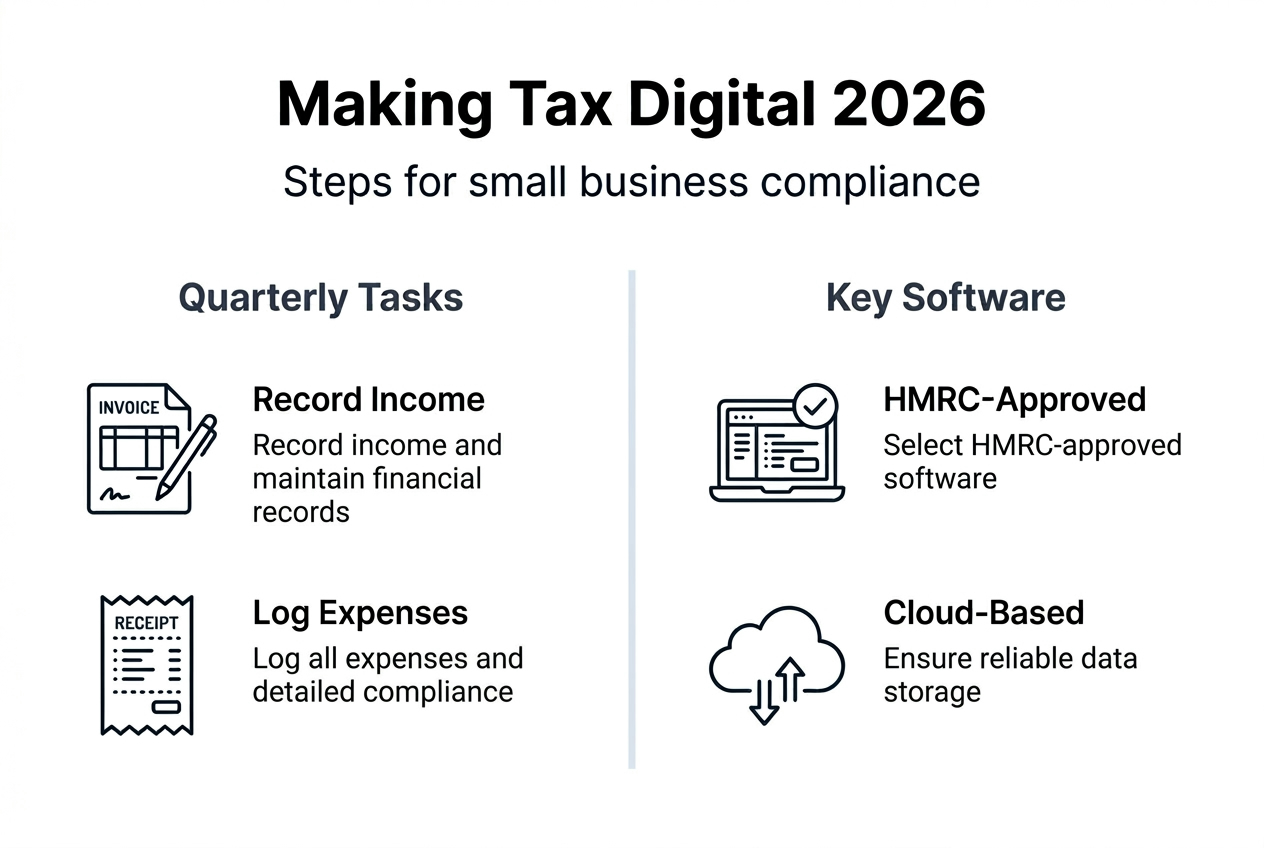

Navigating Making Tax Digital for income tax in 2026

Making Tax Digital for Income Tax launches in phases starting April 2026 for sole traders and landlords earning over £50,000. This replaces annual self-assessment with quarterly digital updates submitted through compatible software. The threshold drops to £30,000 in April 2027, eventually covering most self-employed individuals.

Quarterly updates summarise your income and expenses for each three-month period. You submit these through HMRC-approved software, then file a final declaration after your tax year ends. This spreads tax administration throughout the year rather than concentrating everything into January's self-assessment rush.

Those joining MTD in April 2026 receive no penalty points for late quarterly updates during their first 12 months. After this grace period, late submissions accumulate penalty points. Four points trigger a £200 fine, with additional £200 penalties for each subsequent point until you reach zero points again.

Key MTD requirements include:

- Digital record keeping using compatible software from day one

- Quarterly update submissions within one month of each period ending

- Final declaration submission after your accounting year closes

- Accurate categorisation of income and expenses per HMRC standards

- Retention of digital records for at least five years

Pro Tip: Set quarterly reminders two weeks before each deadline to review records, categorise transactions, and submit updates without rushing, reducing errors that could accumulate penalty points.

The penalty points system resets to zero after 24 months of compliance. This encourages consistent, timely record keeping rather than last-minute preparation. Understanding these changes through review accounting practices 2026 helps you adapt smoothly. Check the complete making tax digital new rules for detailed implementation timelines.

Updates to capital allowances: writing-down allowance and first-year allowance

Capital allowances let you deduct the cost of business assets from your profits before calculating tax. Two significant changes take effect in April 2026: the main rate of Writing-Down Allowance reduces from 18% to 14% for plant and machinery, whilst a new 40% First-Year Allowance encourages investment in qualifying equipment.

The reduced WDA rate means slower annual depreciation deductions. If you purchased £10,000 of equipment under the old system, you claimed £1,800 in year one. Under the new 14% rate, that same equipment generates only £1,400 in first-year deductions. This affects long-term tax planning for businesses holding substantial equipment pools.

The new FYA offers 40% upfront deduction on qualifying main rate expenditure. This creates an immediate tax benefit for businesses investing in new plant and machinery. Purchasing £10,000 of eligible equipment generates a £4,000 deduction in year one, significantly more than the standard WDA rate.

| Allowance Type | Rate | Eligible Assets | Key Benefit |

|---|---|---|---|

| Writing-Down Allowance | 14% | Plant, machinery, business vehicles | Annual depreciation reduces taxable profit over time |

| First-Year Allowance | 40% | New main rate plant and machinery | Immediate substantial deduction encourages investment |

| Annual Investment Allowance | 100% up to £1m | Most plant and machinery | Full cost deduction in year of purchase for qualifying items |

Strategic timing of equipment purchases maximises these allowances. Buying before your accounting year ends captures the deduction for that tax year. Splitting large purchases across years can optimise your effective tax rate if income fluctuates significantly.

Key considerations include:

- FYA applies only to new, unused assets purchased after April 2026

- Annual Investment Allowance remains at £1 million for most purchases

- Special rate pool items like integral building features use different rates

- Cars have separate allowance rules based on CO2 emissions

- Timing purchases around year-end maximises immediate tax benefits

Pro Tip: Calculate whether claiming FYA or AIA provides better tax outcomes based on your profit level and other allowances available, as you cannot claim both on the same asset.

These changes support unincorporated businesses and leasing providers investing in growth. Detailed guidance on capital allowances changes 2026 clarifies which assets qualify for each allowance rate. Integrate this knowledge with corporate tax planning strategies 2026 for comprehensive tax reduction.

Keeping accurate records and spreading tax administration throughout the year

Keeping accurate records supports every expense claim and ensures MTD compliance. Digital record keeping becomes mandatory under Making Tax Digital, requiring compatible software that tracks income and expenses in real time. This eliminates last-minute scrambling through receipts and bank statements.

Organised records separate business and personal transactions clearly. Open a dedicated business bank account to simplify tracking. Photograph receipts immediately and store them digitally with transaction descriptions. Categorise expenses weekly rather than quarterly to maintain accuracy and spot errors early.

Spreading tax administration throughout the year reduces stress and improves accuracy. Quarterly MTD submissions force regular review of your financial position. This prevents unpleasant surprises in January and helps you plan for tax payments through the year.

Best practices for record keeping include:

- Use cloud-based accounting software compatible with MTD requirements

- Scan and categorise receipts on the day of purchase

- Reconcile bank statements monthly to catch missing transactions

- Tag expenses with appropriate categories matching HMRC standards

- Review quarterly summaries before submitting MTD updates

- Back up financial records to multiple secure locations

Proactive tax planning identifies opportunities before your year ends. Regular review of your profit and expenses lets you time deductible purchases strategically. Quarterly check-ins with your accountant ensure you claim all available allowances and meet compliance requirements.

Managing tax obligations quarterly rather than annually transforms a dreaded annual chore into a manageable routine that improves your financial visibility and control throughout the year.

Pro Tip: Schedule a monthly 30-minute review session to categorise transactions, check for missing receipts, and update your accounting software, preventing the backlog that leads to errors and penalties.

Integrating these practices with vat accounting step by step creates a comprehensive compliance system. The business tax preparation guide provides additional strategies for avoiding common mistakes. Research on start-up tax obligations data confirms that proper preparation prevents costly errors.

Expert accountancy support to maximise your 2026 tax savings

Navigating 2026's tax changes whilst running your business creates competing demands on your time and expertise. Professional guidance ensures you claim every legitimate deduction, meet MTD requirements, and optimise capital allowances without risking compliance errors.

LS25 Accountants specialises in small business tax planning and Making Tax Digital compliance across the LS25 postcode area. We provide personalised advice on allowable expenses, help structure capital allowance claims for maximum benefit, and handle quarterly filing requirements so you can focus on growing your business. Our team stays current on every regulatory change affecting sole traders and small businesses, translating complex rules into actionable strategies that reduce your tax liability legally and effectively. Contact us to review your 2026 tax position and discover opportunities you might be missing. Explore tailored guides and expert insights through LS25 Accountants expert guides for ongoing support throughout the year.

Frequently asked questions

What are allowable expenses for small businesses?

Allowable expenses include office supplies, business travel, marketing costs, professional insurance, and equipment necessary for your operations. You must keep accurate records with receipts and invoices to support each claim and prove business purpose to HMRC.

How will Making Tax Digital affect sole traders in 2026?

Sole traders earning over £50,000 annually must submit quarterly digital updates starting April 2026 instead of one annual return. This spreads tax administration over the year and reduces last-minute errors, though it requires compatible accounting software and regular record keeping.

What changes should I know about capital allowances in 2026?

The writing-down allowance rate decreases from 18% to 14% for main rate assets purchased after April 2026. A new 40% first-year allowance encourages investment in new plant and machinery, offering larger upfront deductions than the reduced WDA rate.

Do I need special software for Making Tax Digital?

You must use HMRC-approved software to keep digital records and submit quarterly updates. Many affordable cloud-based accounting packages meet MTD requirements and include features for expense tracking, invoicing, and automated tax calculations.

What happens if I miss a quarterly MTD deadline?

Businesses joining MTD in 2026 receive a 12-month grace period with no penalty points for late submissions. After this period, you accumulate points for each late submission, receiving a £200 fine after four points and additional penalties for subsequent breaches.