Many UK small business owners unknowingly overpay tax because they misunderstand emergency tax codes and VAT regulations. These codes directly determine your PAYE deductions and VAT liability, affecting cash flow and compliance. This guide clarifies 2026 tax codes and VAT rules, helping you manage finances accurately, avoid costly errors, and stay compliant with HMRC requirements throughout the year.

Table of Contents

- How UK Tax Codes Work And 2026 Updates

- Understanding VAT Codes And Their Impact On Business Accounting

- Key VAT Regulatory Changes For 2026

- Common Misconceptions And Errors In Understanding Tax Codes And VAT

- Applying And Updating Tax Codes In Payroll And Accounting Systems

- Importance Of Compliance And Penalties For Errors

- How LS25 Accountants Support Your Tax And VAT Compliance

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Tax codes determine PAYE deductions | Codes like 1257L reflect your £12,570 personal allowance and vary by region with 2026 updates. |

| VAT codes set rates | T1 (20%), T5 (5%), T2 (0% zero-rated), and T3 (0% exempt) impact pricing and accounting accuracy. |

| 2026 brings VAT relief | New rules exclude business charity donations from VAT liability from April 2026. |

| Emergency codes cause errors | Copying week 1 or month 1 codes into new tax years creates payroll mistakes and overpayments. |

| Compliance avoids penalties | Correct tax and VAT handling prevents HMRC fines, interest charges, and operational disruptions. |

Introduction to UK tax codes and VAT

UK tax codes and VAT form the backbone of your business's financial compliance framework. Tax codes tell HMRC and your payroll system how much income tax to deduct from employee wages under PAYE. Each code contains a number representing the tax-free personal allowance and sometimes a prefix indicating the tax region.

VAT, or Value Added Tax, applies to most goods and services you sell. If your business is VAT-registered, you must charge the correct VAT rate, collect it from customers, and report it accurately to HMRC. Getting VAT codes wrong affects your pricing, invoicing, and VAT returns, potentially triggering penalties.

Understanding both systems ensures you:

- Deduct the right amount of tax from wages

- Charge appropriate VAT rates to customers

- Complete accurate VAT returns and payroll submissions

- Maintain healthy cash flow without unexpected tax bills

- Avoid HMRC penalties and enforcement actions

With 2026 bringing updated personal allowances and new VAT reliefs, staying current protects your business. Tax codes and VAT rules evolve, so regular review keeps you compliant. Mastering these concepts gives you control over your financial obligations and confidence in your accounting accuracy.

Pro Tip: Review your tax codes and VAT settings each April when the new tax year starts to catch any HMRC changes early.

How UK tax codes work and 2026 updates

UK tax codes combine numbers and letters to communicate your tax-free allowance and special circumstances. The numeric part shows your personal allowance divided by 10. For 2026/27, the personal allowance remains £12,570, so the standard code is 1257L.

Prefixes indicate regional differences. Scotland uses 'S' (S1257L), Wales uses 'C' (C1257L), and England/Northern Ireland have no prefix. These regional tax codes reflect devolved tax powers, with Scotland having different income tax bands and rates.

Emergency tax codes like 1257L W1 or 1257L M1 ignore previous earnings in the tax year. They calculate tax only on current pay, often causing overpayment. You receive an emergency code when HMRC lacks full information about your income, such as starting a new job without a P45.

Multiple jobs or pensions affect code assignment. Your main income source gets the full personal allowance code. Secondary incomes receive BR (basic rate, 20% on all earnings), D0 (higher rate, 40%), or D1 (additional rate, 45%) codes with no allowance.

Common tax code elements:

- L: Standard personal allowance applies

- M: Marriage allowance transferred from spouse

- N: Marriage allowance transferred to spouse

- T: Other calculations affect your code

- BR: Basic rate on all income, no allowance

- 0T: Personal allowance used up or removed

| Code type | Tax treatment | When used |

|---|---|---|

| 1257L | Standard allowance £12,570 | Most employees with one job |

| 1257L W1/M1 | Emergency, non-cumulative | New job, missing P45 |

| BR | 20% on all earnings | Second job or pension |

| 0T | No allowance, taxed from £0 | Allowance exhausted |

Pro Tip: If you spot an unexpected emergency code on your payslip, contact HMRC immediately to request a cumulative code and avoid overpaying tax.

Checking your tax code annually prevents errors. HMRC sends P2 notices when codes change. Update your payroll system promptly to reflect new codes and ensure accurate deductions. For detailed guidance on master payroll and tax processes, explore comprehensive resources.

Review the 2026 UK tax codes official guide each spring to understand any adjustments affecting your employees.

Understanding VAT codes and their impact on business accounting

VAT codes classify transactions by VAT rate, directly affecting how you price goods, invoice customers, and complete VAT returns. Each code corresponds to a specific rate and determines which boxes on your VAT return receive the figures.

Standard rate (T1) applies 20% VAT to most goods and services. This is the default for items not qualifying for reduced, zero, or exempt rates. When you sell something at standard rate, you charge 20% VAT, collect it from the customer, and report it in box 1 (VAT amount) and box 6 (net sales) of your VAT return.

Reduced rate (T5) charges 5% VAT on specific items like children's car seats, home energy, and certain renovations. Zero-rated (T2) applies 0% VAT to essentials like most food, books, and children's clothing. You charge no VAT but can reclaim input VAT on purchases.

Exempt (T3) also shows 0% but differs critically from zero-rated. Exempt categories include insurance and finance, where you charge no VAT and cannot reclaim input VAT. This distinction affects profitability and cash flow.

Common VAT rate categories:

- Standard rate 20%: Electronics, furniture, professional services, most retail goods

- Reduced rate 5%: Domestic fuel, energy-saving materials, mobility aids

- Zero-rated 0%: Food (unprocessed), books, newspapers, public transport

- Exempt 0%: Financial services, insurance, education, healthcare

VAT codes impact your accounting by determining:

- Invoice totals and customer pricing

- VAT return box allocations

- Input VAT recovery eligibility

- Profit margins after VAT treatment

| VAT code | Rate | Box 1 (VAT) | Box 6 (Sales) | Input VAT recovery |

|---|---|---|---|---|

| T1 | 20% | Yes | Yes | Yes |

| T5 | 5% | Yes | Yes | Yes |

| T2 | 0% | No | Yes | Yes |

| T3 | 0% | No | No | No |

Choosing the wrong VAT code creates errors in VAT return reporting, potentially triggering HMRC queries. If you misclassify standard-rated sales as exempt, you underpay VAT and face penalties. Misclassifying zero-rated as exempt means you lose input VAT recovery, increasing costs.

For step-by-step guidance on VAT accounting step by step, consult detailed resources tailored to UK businesses.

Review the VAT codes and returns guide to understand how coding affects your compliance.

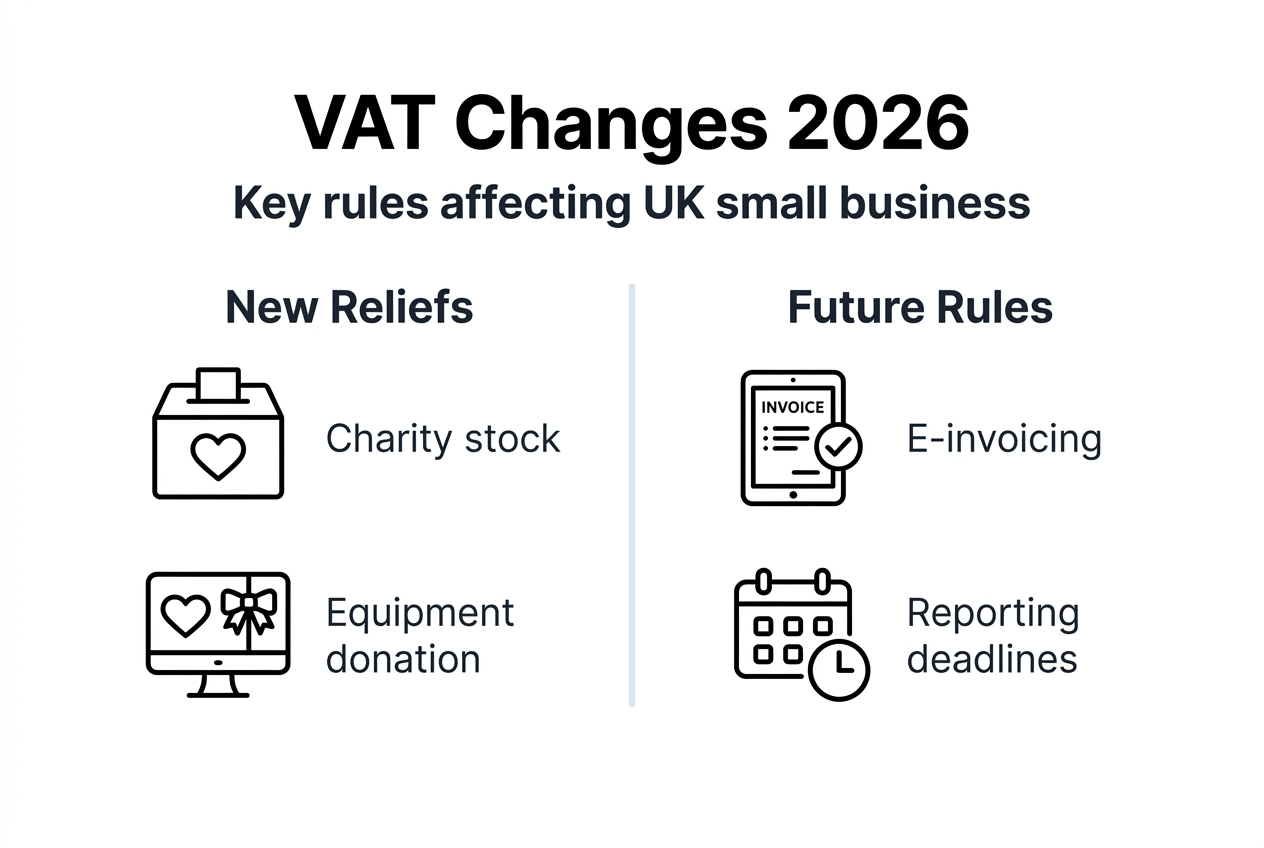

Key VAT regulatory changes for 2026

2026 brings significant VAT updates affecting UK small businesses. The most immediate change is VAT relief for charity donations starting April 2026. Previously, donating business goods to charity created a deemed supply, triggering VAT liability. The new relief removes this charge, encouraging charitable giving without tax penalties.

This change means if you donate surplus stock or equipment to registered charities, you no longer owe VAT on the deemed sale. It simplifies accounting and reduces your VAT burden when supporting community causes.

Looking ahead, HMRC plans mandatory electronic invoicing by 2029. While implementation is three years away, preparation starts now. Electronic invoicing will require digital formats meeting HMRC standards, increasing compliance requirements and accelerating digitisation.

Other 2026 indirect tax updates include refined rules for cross-border e-commerce and adjustments to place-of-supply rules for digital services. If you sell goods or services internationally, these changes affect VAT treatment and registration thresholds.

Immediate actions to prepare:

- Review your charity donation processes and accounting treatment

- Audit current invoicing systems for digital readiness

- Consult with tax advisors on international VAT obligations

- Update accounting software to handle new VAT relief codes

- Train staff on 2026 VAT rule changes and documentation requirements

Pro Tip: Schedule a consultation with a VAT specialist in early 2026 to review your business's exposure to these changes and implement adjustments before penalties arise.

Staying ahead of regulatory shifts protects your business from non-compliance risks. For broader guidance on small business accounting tips, explore resources covering payroll, VAT, and tax management.

Read the full 2026 VAT regulatory changes analysis to understand how these updates affect your sector.

Common misconceptions and errors in understanding tax codes and VAT

Small businesses frequently confuse zero-rated and exempt VAT categories. Both show 0% VAT on invoices, but the difference is critical. Zero-rated items like bread or books allow you to reclaim input VAT on related purchases. Exempt services like insurance and education prevent input VAT recovery, increasing your costs.

Misclassifying exempt as zero-rated means you wrongly reclaim VAT, triggering HMRC corrections and potential penalties. Misclassifying zero-rated as exempt costs you money by forfeiting legitimate VAT recovery.

Another common error involves carrying forward week 1 or month 1 tax codes from previous years. These non-cumulative codes calculate tax only on current period pay, ignoring earlier earnings. Using them beyond their intended short-term purpose causes persistent overpayment or underpayment.

Emergency tax codes also create confusion. Many assume emergency codes correct themselves automatically. In reality, you must provide HMRC with accurate information or request a code change. Waiting passively means continued incorrect deductions.

Employers sometimes apply the wrong regional prefix, using English codes for Scottish employees or vice versa. This error misstates tax liability because Scotland has different income tax bands.

Typical misconceptions and corrections:

- Myth: All 0% VAT is the same. Reality: Zero-rated allows input VAT recovery; exempt does not.

- Myth: Emergency codes self-correct. Reality: You must contact HMRC or provide a P45 to update codes.

- Myth: Tax codes never change mid-year. Reality: HMRC issues new codes anytime circumstances change.

- Myth: VAT registration is optional under the threshold. Reality: Voluntary registration is allowed and sometimes beneficial.

- Myth: One tax code covers all income. Reality: Multiple jobs require different codes per income source.

Verify your tax codes each April and whenever you receive HMRC notifications. Check VAT treatment for each product or service you sell, consulting official guidance when uncertain. For help avoiding errors, review the business tax preparation guide to catch common mistakes before they cost you.

Consult VAT rates official guidance to confirm correct classification for your offerings.

Applying and updating tax codes in payroll and accounting systems

Applying tax codes correctly in your payroll system ensures accurate PAYE deductions and compliance. Follow these steps each time you process payroll or receive updated codes from HMRC.

- Review current tax codes before each payroll run, checking for HMRC notifications or employee P45/P46 forms providing new codes.

- Assign the correct code to each employee based on their circumstances, ensuring regional prefixes match their residence.

- Remove any week 1 or month 1 markers unless HMRC specifically instructs otherwise, as carrying these forward causes errors.

- Process payroll using updated codes, double-checking calculations for employees with code changes.

- Monitor payroll reports for anomalies like unexpectedly high or low deductions, which signal incorrect codes.

When HMRC sends a new tax code notification, act immediately. Update your payroll system within the next pay period to avoid underpaying or overpaying tax. If an employee starts work without providing a P45, use the emergency code 1257L W1 or M1 temporarily, then update once you receive proper documentation.

Pro Tip: Enable alerts in your payroll software to flag discrepancies between assigned codes and expected deductions, catching errors before submission.

Regular monitoring prevents small mistakes from becoming large problems. Review payroll summary reports after each run, comparing total deductions against expected amounts. If figures seem off, audit individual employee codes immediately.

For comprehensive guidance on audit payroll compliance, explore resources covering payroll accuracy and error prevention.

Maintaining accurate codes year-round protects both your business and employees from tax complications. Check the official 2026 tax code guidance whenever you have questions about correct application.

Importance of compliance and penalties for errors

HMRC prioritises reducing the tax gap through targeted enforcement and audits. Incorrect tax codes and VAT misreporting draw scrutiny, potentially triggering investigations that disrupt operations and damage reputations.

Financial penalties for VAT errors range from simple interest charges to substantial fines. If HMRC determines you carelessly or deliberately reported incorrect VAT, penalties reach 100% of the tax owed or more. Even innocent mistakes incur interest from the date VAT was due.

Incorrect tax codes create problems for employees and employers. Employees face unexpected tax bills or delays in refunds. Employers risk penalties for failing to operate PAYE correctly, plus the administrative burden of corrections.

Operational disruptions from non-compliance include:

- HMRC compliance checks requiring extensive documentation and time

- Cash flow strain from paying backdated tax, interest, and penalties

- Reputational damage affecting customer and supplier relationships

- Loss of focus on core business activities during audit periods

- Potential legal action for serious or repeated non-compliance

"HMRC continues to invest in sophisticated data analytics and cross-referencing systems to identify discrepancies in VAT returns and PAYE submissions, making accurate reporting more important than ever for small businesses in 2026."

Resources to support compliance:

- HMRC online guidance and webinars on tax codes and VAT

- Professional accountants and tax advisors for complex situations

- Payroll and accounting software with built-in compliance checks

- Industry-specific VAT guidance for specialised sectors

- Regular training for finance staff on regulatory updates

Investing in professional support pays dividends by preventing costly errors. For practical steps to improve accuracy, explore the business tax preparation guide and VAT accounting step-by-step resources.

Regularly review accounting practices to identify weaknesses before they trigger penalties. Consider the tax advisor benefits of expert guidance tailored to your business.

How LS25 Accountants support your tax and VAT compliance

Navigating 2026 tax codes and VAT regulations becomes simpler with expert support. LS25 Accountants specialise in helping UK small businesses achieve accuracy in PAYE, VAT returns, and financial reporting. Their team understands the nuances of regional tax codes, VAT rate classifications, and the latest regulatory changes affecting your business.

Whether you need help implementing the new VAT relief for charity donations or updating payroll systems for 2026 tax codes, LS25 Accountants provide tailored guidance. Their practical approach reduces errors, prevents penalties, and gives you confidence in your compliance.

Explore LS25 Accountants expert services to discover how personalised accounting support protects your business. For ongoing learning, review their business tax preparation guide and small business accounting tips to stay ahead of compliance requirements throughout 2026 and beyond.

Frequently asked questions

What is a tax code and how does it affect my business?

A tax code tells HMRC how much income tax to deduct from employee wages under PAYE. It reflects the personal allowance and adjustments like benefits or multiple jobs. Using correct codes ensures accurate tax payment, avoiding overpayments or underpayments that disrupt cash flow and compliance.

How do VAT codes impact my business accounting?

VAT codes determine the VAT rate applied to each transaction, affecting invoice totals and VAT return accuracy. Correct codes ensure you charge appropriate VAT, report it in the right boxes, and recover input VAT where eligible. Errors lead to compliance issues and potential penalties.

What should I do if I receive a new tax code from HMRC?

Review the new code immediately to understand why it changed. Update your payroll system before the next pay run to apply the code correctly. If the code seems wrong, contact HMRC to clarify. For detailed guidance, explore audit payroll compliance resources to maintain accuracy.

Why is it important to avoid copying week 1 or month 1 tax codes from previous years?

Week 1 or month 1 codes calculate tax non-cumulatively, ignoring earlier pay in the tax year. Carrying these codes forward causes persistent overpayment or underpayment because they do not account for the full year's earnings. Always use cumulative codes unless HMRC specifies otherwise.