Cash flow problems affect 82% of UK SMEs, yet many business owners still rely solely on profit figures to gauge financial health. Profitability does not guarantee survival. A profitable company can collapse if cash runs out at the wrong moment. Cash flow forecasting is a vital financial tool that predicts when money enters and leaves your business, helping you avoid painful shortages and plan growth confidently. Despite its importance, many UK businesses underuse or misunderstand this practice. This guide explains what cash flow forecasting is, why it matters for your business survival, and how to implement it effectively to strengthen your financial position and secure your future.

Table of Contents

- Understanding Cash Flow Forecasting And Its Importance

- The Benefits Of Cash Flow Forecasting For Uk Businesses

- Addressing Common Cash Flow Forecasting Challenges And Nuances

- How To Implement An Effective Cash Flow Forecast In Your Business

- Explore Expert Cash Flow And Accounting Support With Ls25 Accountants

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Predicts cash timing | Cash flow forecasting shows when money comes in and goes out, not just total profit |

| Improves funding success | Regular forecast updates increase loan approval rates by helping lenders see organised planning |

| Reduces cash cycle time | Effective forecasting helps manage working capital and can cut cash cycle time by around 15% |

| Warns of shortages early | Forecasts alert you to payment delays and potential cash gaps before they become crises |

| Supports growth planning | Clear cash visibility enables confident decisions about expansion, hiring, and investment |

Understanding cash flow forecasting and its importance

A cash flow forecast predicts how much money you expect to come in and go out over a specific time period, usually 12 months. It tracks the actual movement of cash through your business accounts, showing when funds will be available for expenses, investments, or emergencies. This forward-looking view helps you anticipate shortages and surpluses, allowing proactive financial management rather than reactive crisis handling.

Many business owners confuse cash flow with profit, but they measure fundamentally different things. Profit shows your overall earnings after deducting costs, appearing on your profit and loss statement. Cash flow focuses on timing of cash movements, revealing when money physically enters or leaves your bank account. You might record a sale today that contributes to profit, but if the customer pays in 60 days, that cash is not available now for payroll or rent. This timing gap creates the cash flow challenge.

Timing matters enormously because businesses operate in real time with immediate obligations. Your suppliers expect payment on agreed dates. Staff need wages on schedule. Rent comes due monthly regardless of when customers pay you. A business can show healthy profits on paper whilst simultaneously struggling to meet basic expenses due to delayed receivables or seasonal fluctuations. Running out of cash is one of the most common reasons UK businesses fail, even profitable ones.

The risks of poor cash flow extend beyond inconvenience. Insolvency occurs when you cannot pay debts as they fall due, regardless of your profit position. Late payments to suppliers damage relationships and creditworthiness. Missed payroll destroys staff morale and retention. Emergency borrowing at unfavourable rates erodes profitability. Understanding managing cash flow in your business prevents these cascading problems.

A basic cash flow forecast includes several essential components:

- Opening balance: cash available at the start of the forecast period

- Expected receipts: all anticipated cash inflows from sales, investments, loans, or other sources

- Planned payments: all expected cash outflows including suppliers, wages, rent, taxes, and loan repayments

- Closing balance: opening balance plus receipts minus payments, showing predicted cash position

- Variance analysis: comparing forecasted figures against actual results to improve future accuracy

Pro Tip: Treat your cash flow forecast as a living document. Update it weekly or monthly with actual figures to spot trends early and adjust predictions based on real performance rather than outdated assumptions.

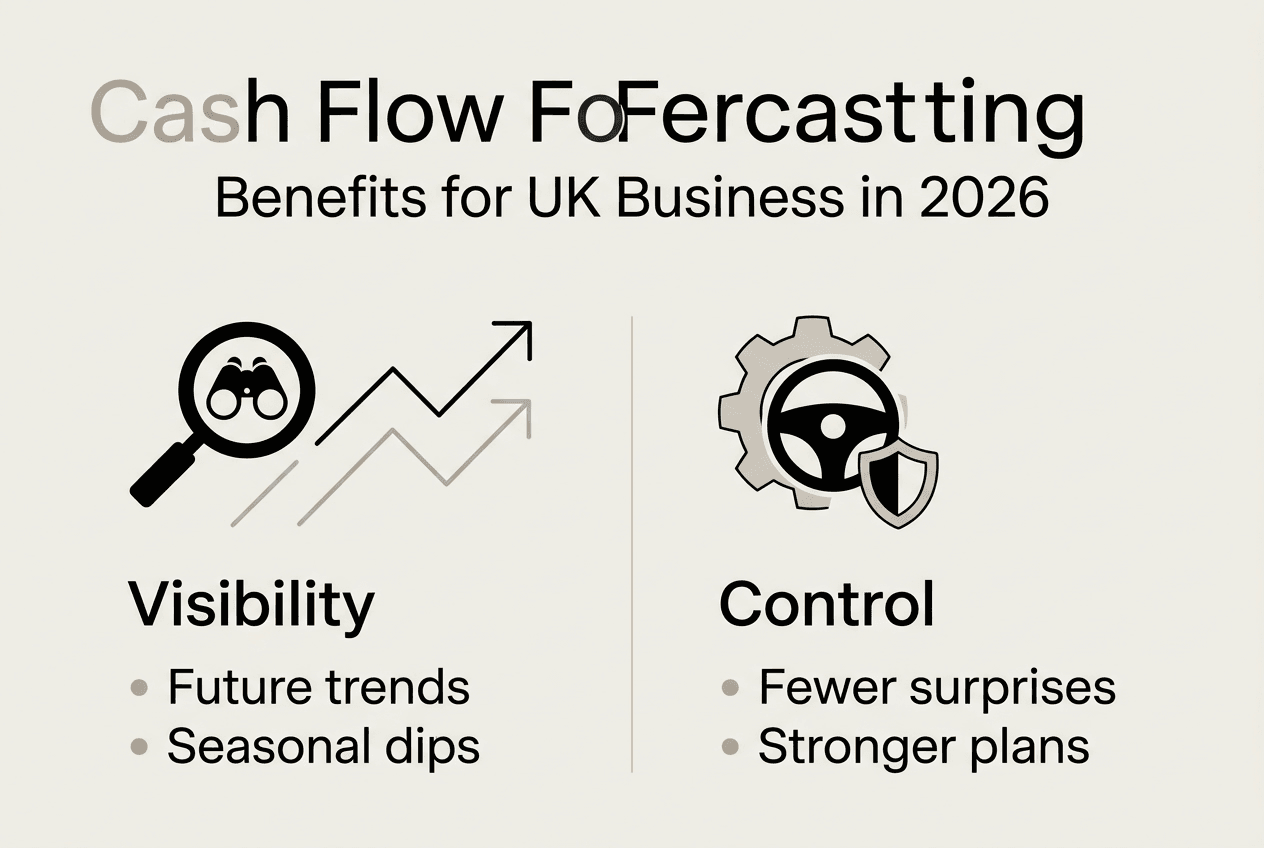

The benefits of cash flow forecasting for UK businesses

Cash flow forecasting transforms how you plan and operate your business by providing visibility into future financial positions. The ability to see potential shortages weeks or months ahead allows you to take preventive action, whether that means chasing overdue invoices, negotiating extended payment terms with suppliers, or arranging temporary financing. This forward planning eliminates the stress and cost of last-minute crisis management.

Lenders and investors value organised financial planning. Businesses updating forecasts monthly show 15% higher success in securing funding because they demonstrate financial competence and control. When you approach a bank with a detailed, regularly updated cash flow forecast, you prove you understand your business finances and can manage borrowed funds responsibly. This credibility often makes the difference between loan approval and rejection.

Working capital optimisation becomes possible when you understand cash timing patterns. Forecasting helps reduce working capital cycle by an average of 15% through better management of receivables, payables, and inventory. You can identify when to chase slow-paying customers, when to take early payment discounts from suppliers, and when excess cash allows inventory investment. These marginal gains compound into significant competitive advantages.

Financial control improves dramatically with regular forecasting. Cash flow forecasting helps spot financial issues early, plan growth, and make smarter decisions by revealing patterns and trends invisible in monthly accounting statements. You gain the confidence to cut non-essential expenses before they become problematic, invest in growth opportunities when cash permits, and avoid overcommitting resources during tight periods. Implementing effective cash flow management strategies builds on this foundation.

Key benefits of regular cash flow forecasting include:

- Early detection of potential cash shortages allowing proactive solutions

- Better collection management by highlighting which customers need chasing

- Improved supplier relations through reliable, timely payments that may unlock discounts

- Support for growth investments by identifying when surplus cash enables expansion

- Enhanced credibility with lenders, investors, and business partners

- Reduced financial stress through greater certainty and control

Pro Tip: Update your forecasts at least monthly, but consider weekly updates during periods of rapid change or growth. Market conditions shift quickly, and frequent updates help you seize funding opportunities or avoid emerging risks that quarterly reviews might miss.

Addressing common cash flow forecasting challenges and nuances

Late payments represent one of the most significant challenges to accurate cash flow forecasting and business survival. 62.6% of invoices are paid late across the UK, costing £2 billion annually to the economy. These delays create a domino effect, forcing businesses to delay their own payments, seek expensive short-term financing, or deplete reserves meant for growth and emergencies.

The scale of the late payment problem affects forecasting accuracy and business viability:

| Metric | Figure | Source |

|---|---|---|

| Invoices paid late | 62.6% | Financial IT 2026 |

| Average late payment owed | £21,400 per SME | QuickBooks 2025 |

| Annual cost to UK businesses | £2 billion | Financial IT 2026 |

| SMEs closing annually due to cash flow | 50,000 | Equifax UK 2026 |

The average SME is owed £21,400 in late payments, representing a substantial portion of working capital tied up unproductively. Approximately 50,000 SMEs close annually due to cash flow problems, many directly caused by late payments from larger customers who exploit extended terms.

Seasonal fluctuations add another layer of complexity to cash flow forecasting. Retail businesses experience peaks around holidays, construction firms face weather-related slowdowns, and professional services may see summer dips. These predictable patterns require different forecasting approaches than steady-state businesses, with careful planning for lean periods and strategic reserves built during peak seasons.

Practical steps to address forecasting challenges and improve accuracy:

- Implement rolling forecasts that extend 12 months forward and update monthly, replacing outdated periods with new projections based on actual performance and current market conditions.

- Chase invoices proactively by contacting customers before payment due dates, sending reminders immediately when payments are late, and escalating collection efforts systematically.

- Negotiate payment terms that balance customer relationships with cash flow needs, offering early payment discounts or requesting deposits for large orders.

- Build cash reserves during strong periods to buffer against seasonal dips, unexpected expenses, or customer payment delays without resorting to expensive emergency borrowing.

- Monitor forecasts frequently, comparing predicted versus actual figures weekly or monthly to identify variances, understand causes, and refine future predictions.

Integrating your forecast with broader planning, such as a comprehensive tax planning checklist for UK businesses, ensures all financial obligations are anticipated and funded appropriately.

Pro Tip: Use your cash flow forecast not just as a prediction tool but as a management dashboard. When forecasts show tightening cash positions, immediately review discretionary spending, accelerate collections, and delay non-essential payments to maintain liquidity without crisis.

How to implement an effective cash flow forecast in your business

Creating your first cash flow forecast requires gathering historical financial data and making informed projections about future activity. Start by collecting bank statements, sales records, supplier invoices, and any recurring payment obligations from the past 12 months. This historical data reveals patterns in revenue timing, seasonal fluctuations, and typical payment cycles that inform realistic future projections.

Estimate receipts by reviewing your sales pipeline, existing contracts, and historical conversion rates. Break down expected cash inflows by source and timing, accounting for payment terms. If customers typically pay 30 days after invoicing, factor that delay into your forecast rather than assuming immediate payment. Be conservative with revenue projections, especially for new products or uncertain economic conditions.

Estimate payments by listing all anticipated outflows including supplier costs, wages, rent, utilities, loan repayments, tax obligations, and discretionary spending. Fixed costs are straightforward to predict. Variable costs require estimation based on expected activity levels. Include annual or quarterly payments that might be overlooked in monthly accounting, such as insurance premiums, professional subscriptions, or tax bills.

Set your forecast period to cover at least 12 months, broken into monthly intervals. This timeframe captures seasonal variations and annual cycles whilst remaining manageable to maintain. Some businesses benefit from weekly forecasts for the next quarter combined with monthly projections for the remaining nine months, providing detailed short-term visibility with longer-term planning.

Maintaining forecast accuracy requires regular updates with actual results. Each month, compare your predicted receipts and payments against what actually occurred. Investigate significant variances to understand whether they represent one-time events or systematic forecasting errors. Adjust future projections based on these learnings, creating a continuous improvement cycle that increases accuracy over time.

Payment terms strategies significantly impact cash flow and sales performance. Businesses requesting immediate payment report 5% sales growth versus 2% for those with 90-day terms, demonstrating that tighter payment terms can actually boost revenue whilst improving cash flow. Consider offering early payment discounts or implementing deposits for large orders to accelerate cash collection.

Best practices for effective cash flow forecasting:

- Include all cash inflows and outflows, not just major items, because small recurring expenses accumulate into significant amounts that can derail forecasts if omitted.

- Update forecasts monthly at minimum, incorporating actual results and adjusting future predictions based on current business conditions and market trends.

- Review variances systematically, investigating why predictions differed from reality and using those insights to refine estimation methods and assumptions.

- Plan contingencies by maintaining a buffer between projected closing balance and zero, accounting for unexpected expenses or delayed receipts without triggering overdrafts.

- Use software or tools designed for cash flow forecasting rather than basic spreadsheets, as dedicated solutions automate calculations, highlight trends, and reduce errors.

Connecting your cash flow forecast with your overall financial planning creates a comprehensive management system. Learn more through this detailed business budgeting guide for 2026 that explains how budgets and forecasts work together.

Pro Tip: Link your cash flow forecast directly with your budgeting process for comprehensive financial planning. Whilst budgets set spending limits and targets, cash flow forecasts ensure the timing of those activities aligns with available funds, preventing budget compliance that still creates cash shortages.

Explore expert cash flow and accounting support with LS25 Accountants

Cash flow forecasting delivers powerful benefits, but creating and maintaining accurate forecasts requires time, expertise, and discipline that many business owners struggle to sustain alongside operational demands. Professional accountants simplify the forecasting process whilst improving accuracy through experience across multiple businesses and industries. They spot patterns and risks that inexperienced forecasters miss, helping you avoid costly mistakes.

LS25 Accountants offers expert guidance and practical tools customised to businesses across the LS25 postcode area, combining local knowledge with professional accounting expertise. Our team helps you build robust forecasting systems, interpret results, and translate financial data into actionable business decisions. Access to ongoing support ensures your forecasts remain current and effective as your business evolves and market conditions change. Visit LS25 Accountants to explore our resources, read expert articles on financial management, and contact our advisers for personalised support that strengthens your cash flow management and overall financial health.

FAQ

What is the ideal frequency for updating a cash flow forecast?

Update your cash flow forecast at least monthly, replacing actual results and extending projections forward. Businesses experiencing rapid growth, seasonal fluctuations, or cash constraints benefit from weekly updates that provide earlier warning of emerging issues and opportunities.

How can I handle unpredictable late payments in my forecast?

Build payment delay assumptions into your forecast based on historical customer behaviour, adding 10 to 20 days to stated payment terms for customers with poor payment records. Maintain a cash buffer to absorb delays without triggering shortages, and implement proactive collection procedures to minimise late payments.

Can cash flow forecasting help me secure a business loan?

Yes, lenders view regularly updated cash flow forecasts as evidence of financial competence and control, significantly improving loan approval chances. A detailed forecast demonstrates you understand your cash needs, can manage borrowed funds responsibly, and have planned repayment capacity.

What software tools are recommended for small UK businesses?

Popular options include Xero, QuickBooks, and FreeAgent, which integrate bank feeds, automate calculations, and generate forecast reports. Choose software that matches your business complexity and integrates with existing accounting systems for seamless data flow and reduced manual entry.

How does cash flow forecasting differ from budgeting?

Budgeting sets spending limits and revenue targets for a period, focusing on what you plan to achieve. Cash flow forecasting predicts when money moves in and out, focusing on timing and liquidity. Budgets guide decisions; forecasts ensure those decisions align with available cash.