Many LS25 small businesses face a troubling reality: healthy profits on paper yet persistent cash shortages threatening operations. Late payments, seasonal fluctuations, and timing mismatches between income and expenses create crises that force otherwise viable businesses to close. This guide delivers practical, proven strategies to help LS25 business owners and sole traders master cash flow management, maintain financial stability, and meet evolving compliance requirements including Making Tax Digital mandates effective April 2026.

Table of Contents

- Understanding Cash Flow And Common Challenges

- Preparing Effective Cash Flow Forecasts

- Practical Cash Flow Management Strategies

- Ensuring Compliance With Accounting And Tax Regulations

- Find Expert Cash Flow Support In LS25

- Frequently Asked Questions About Cash Flow Management

Key takeaways

| Point | Details |

|---|---|

| Cash flow crisis scale | 82% of UK SMEs face cash issues with £32bn owed in late payments annually |

| Essential forecasting | 13-week rolling forecasts updated weekly enable proactive decisions for volatile businesses |

| Immediate improvements | Invoice within 14-30 days, automate payment reminders, and maintain 2-3 months operating reserves |

| Compliance simplification | Cash basis accounting aligns tax reporting with actual cash movements for sole traders |

| Technology advantage | Cloud accounting software reduces errors and automates tracking for better visibility |

Understanding cash flow and common challenges

Cash flow represents money moving through your business: inflows from sales, loans, and investments versus outflows for expenses, taxes, and repayments. Unlike profit calculations that recognise income when earned, cash flow management tracks timing of actual money received and paid. This distinction proves critical because businesses can show strong profits whilst experiencing insolvency from timing mismatches.

The reality for LS25 businesses mirrors broader UK challenges. Research shows 82% of SMEs experience cash flow difficulties, with 62.6% of invoices paid late and average delays reaching 21-62 days. Small businesses collectively face £32bn in outstanding late payments, contributing to 50,000 annual closures driven primarily by cash flow failures rather than unprofitability. These statistics reveal a systemic problem requiring proactive management.

Working capital, the difference between current assets and liabilities, determines your operational buffer. Insufficient reserves force difficult choices: delaying supplier payments, missing growth opportunities, or facing penalties. Understanding why cash flow forecasts matter helps prevent these scenarios through advance planning.

Common cash flow challenges include:

- Late customer payments creating unpredictable income timing

- Seasonal revenue fluctuations requiring reserves for lean periods

- Overtrading where rapid growth outpaces available cash

- Fixed overhead costs continuing during revenue downturns

- Tax payment deadlines requiring large lump sums

- Inventory investments tying up cash before sales occur

Recognising these patterns early enables targeted interventions before crises develop.

Preparing effective cash flow forecasts

Accurate forecasting transforms reactive crisis management into proactive financial control. The 13-week rolling forecast updated weekly provides optimal visibility for businesses facing volatility. This timeframe balances detail with practicality, allowing you to anticipate short-term needs whilst maintaining manageable data requirements.

Three primary methodologies serve different business situations. The direct method tracks actual cash receipts from customers and payments to suppliers, offering precise visibility into real money movements. The indirect method starts with profit figures then adjusts for non-cash items like depreciation and changes in working capital. Driver-based forecasting links cash flow projections to operational metrics such as sales volume, average payment days, and inventory turnover.

| Method | Ease of Use | Accuracy | Best For |

|---|---|---|---|

| Direct | Moderate | High | Businesses with simple transactions |

| Indirect | Complex | Moderate | Companies using accrual accounting |

| Driver-based | High | Very High | Businesses with predictable patterns |

For LS25 sole traders and small businesses, the direct method typically provides the clearest picture without requiring complex accounting knowledge. You simply track when money actually arrives and leaves your bank account, matching the cash basis approach many sole traders already use for tax purposes.

Driver-based models excel when you identify reliable operational indicators. If you know customers typically pay within 35 days and suppliers grant 45-day terms, you can project cash timing from sales forecasts. This approach helps you model scenarios: what happens if sales increase 20% or payment delays extend to 45 days?

Implementing effective cash flow management strategies requires selecting the right forecasting method for your business complexity and data availability. Start simple, then refine as you gather historical patterns.

Pro Tip: Automate forecast updates using cloud accounting software that pulls transaction data directly from bank feeds, eliminating manual entry errors and saving hours weekly whilst improving accuracy through real-time visibility.

Practical cash flow management strategies

Theory matters little without execution. These proven tactics deliver immediate cash flow improvements when implemented consistently.

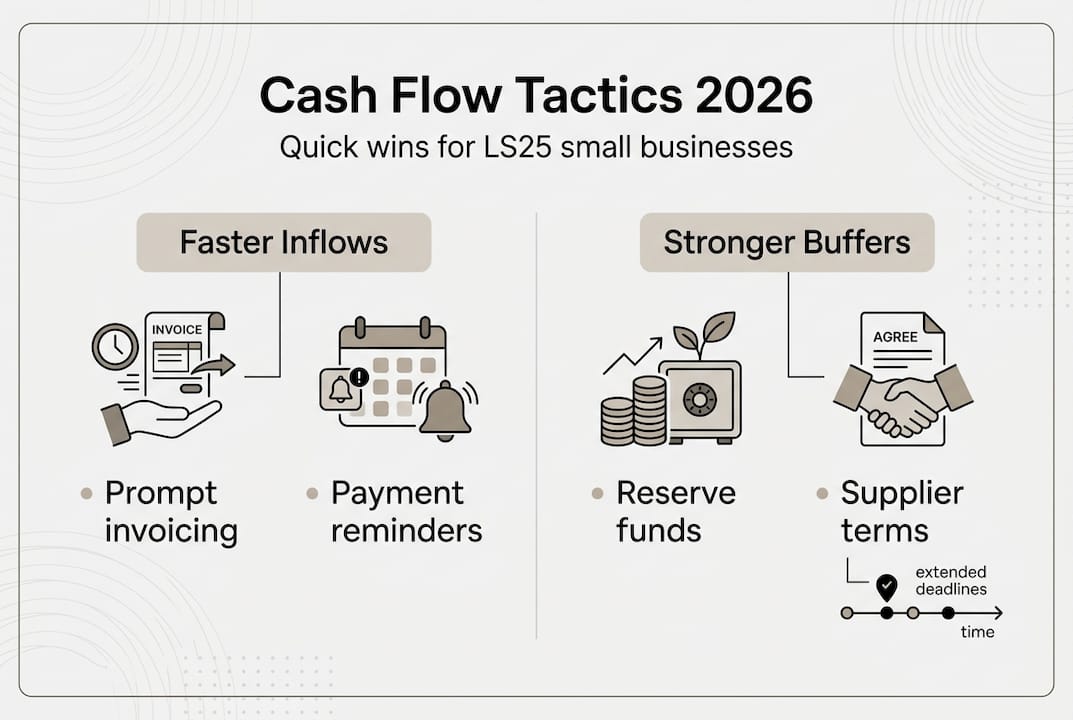

Prompt invoicing accelerates inflows dramatically. Issue invoices within 24 hours of completing work or delivering goods, setting clear payment terms of 14-30 days rather than the traditional 60-90 day periods that create unnecessary delays. Every day you postpone invoicing extends the payment cycle, worsening cash position unnecessarily.

Chasing late payments requires systematic processes, not occasional reminders. Automated payment reminders sent at seven days before due date, on due date, and at seven-day intervals thereafter maintain pressure without consuming your time. Many cloud accounting platforms include this functionality, removing the awkwardness whilst improving collection rates substantially.

Supplier relationship management offers often-overlooked opportunities. Negotiate extended payment terms with key suppliers, aiming for 45-60 days rather than immediate or 30-day terms. This costs nothing yet improves cash timing significantly. Some suppliers offer early payment discounts; calculate whether the percentage saved exceeds your cost of capital before accepting shorter terms.

Building operating reserves equal to 2-3 months of expenses creates essential buffers against unexpected shortfalls. Treat reserve building as a non-negotiable expense, transferring funds monthly into a separate account. This discipline prevents the temptation to spend available cash, ensuring resources exist when seasonal downturns or late payments create temporary gaps.

Technology adoption through platforms like Xero or QuickBooks transforms managing cash flow in your business from spreadsheet guesswork to real-time visibility. Bank feeds update balances automatically, categorisation learns from patterns, and dashboards highlight trends requiring attention.

Key implementation steps include:

- Review cash position daily, not monthly

- Set automatic payment reminders for all invoices

- Negotiate payment terms with top five suppliers

- Transfer fixed percentage of revenue to reserves monthly

- Use accounting software with bank feed integration

- Create contingency plans for 20% revenue drops

Consistency matters more than perfection. Implementing even three of these tactics delivers measurable improvements within weeks.

Pro Tip: Monitor your operating reserve ratio monthly by dividing current reserves by average monthly expenses, targeting a minimum of 2.0 to ensure adequate buffers whilst preparing scenario-based contingency plans for accessing additional funds if reserves approach critical levels.

Ensuring compliance with accounting and tax regulations

Compliance and cash flow management reinforce each other when structured properly. Understanding requirements prevents penalties whilst improving financial visibility.

Cash basis accounting records income when received and expenses when paid, aligning tax reporting with actual cash movements. This approach became the default for sole traders from the 2024/25 tax year, simplifying compliance for businesses with turnover below £150,000. Unlike accrual accounting that recognises income when earned regardless of payment, cash basis matches your bank statements, reducing complexity substantially.

Making Tax Digital requirements take effect April 2026, mandating digital record keeping and online submission for VAT and Income Tax Self Assessment. This shift from paper records and manual returns requires compatible software but offers advantages: reduced errors, real-time visibility, and automated calculations that improve accuracy whilst saving time.

Essential compliance steps for LS25 sole traders include:

- Confirm eligibility for cash basis accounting based on turnover and business type

- Implement digital record keeping using Making Tax Digital compatible software before April 2026

- Submit Self Assessment returns by 31 January following the tax year end

- Maintain detailed records of all income and expenses with supporting documentation

- Retain financial records for minimum five years after submission deadline

Proper compliance improves cash flow visibility by enforcing systematic record keeping. When you track every transaction for tax purposes, you simultaneously build the data foundation for accurate forecasting. Digital systems highlight patterns, flag anomalies, and generate reports that inform better decisions.

Understanding tax compliance requirements for UK businesses prevents penalties that damage cash flow. Late filing penalties start at £100, escalating to £1,600 plus daily charges for extended delays. Late payment interest compounds at 7.75% annually on outstanding balances. These avoidable costs drain resources that could fund operations or reserves.

The cash basis approach particularly benefits businesses with significant timing differences between invoicing and payment. You only pay tax on money actually received, avoiding the cash flow strain of paying tax on unpaid invoices under accrual accounting. This alignment reduces working capital requirements and simplifies forecasting.

Find expert cash flow support in LS25

Managing cash flow effectively requires both systematic processes and expert guidance tailored to your specific circumstances. Professional accountants bring experience across hundreds of businesses, identifying patterns and solutions you might miss whilst navigating alone.

LS25 Accountants specialises in helping local business owners implement practical cash flow strategies that deliver measurable improvements. Our team understands the unique challenges facing LS25 businesses, from seasonal fluctuations to supplier payment terms common in the area. We provide personalised advice on forecasting methods, compliance requirements, and technology selection suited to your operations.

Access expert articles and practical guides covering everything from Making Tax Digital preparation to tax planning strategies that optimise cash timing. Our resources help you implement proven techniques whilst avoiding common mistakes that drain resources unnecessarily.

Whether you need help establishing forecasting systems, ensuring compliance, or resolving immediate cash flow challenges, professional accounting services deliver both technical expertise and strategic perspective. Contact us to discuss how tailored support can strengthen your financial stability and free you to focus on growing your business.

Frequently asked questions about cash flow management

What is the best cash flow forecasting method for small businesses?

The direct method tracking actual receipts and payments works best for most small businesses, offering clear visibility without complex adjustments. Driver-based forecasting provides superior accuracy once you identify reliable operational patterns linking sales to cash timing.

How can I quickly improve cash flow when facing late payments?

Implement automated payment reminders starting seven days before due dates, offer small early payment discounts, and contact customers personally for invoices over 30 days overdue. Consider invoice factoring for immediate cash against outstanding invoices if delays threaten operations.

What records must sole traders keep for Making Tax Digital compliance?

You must maintain digital records of all business income and expenses, supporting documentation like invoices and receipts, and use compatible software for submissions. Records require retention for five years after the 31 January submission deadline.

How often should I update my cash flow forecasts?

Update forecasts weekly for businesses experiencing volatility or growth, rolling forward the 13-week window each time. Stable businesses may update fortnightly, but weekly reviews catch emerging issues before they become crises.

What reserves should a small business hold to remain stable?

Maintain operating reserves covering 2-3 months of fixed expenses as a minimum buffer against unexpected shortfalls. Seasonal businesses or those with volatile income should target 3-6 months, whilst effective cash flow strategies help build these reserves systematically.