Many UK business owners face confusion about tax compliance, especially with Making Tax Digital (MTD) reshaping record-keeping and filing requirements. The transition from traditional paper-based systems to digital platforms creates uncertainty about legal obligations, software choices, and deadlines. This guide clarifies what tax compliance means in 2026, explains MTD requirements for VAT and Income Tax Self Assessment, and provides actionable steps to help your business meet HMRC expectations confidently while avoiding costly penalties.

Table of Contents

- Understanding Tax Compliance For UK Businesses

- Making Tax Digital (Mtd) For Vat: Rules And Deadlines

- Mtd For Income Tax Self Assessment (Itsa): Upcoming Changes For Sole Traders And Landlords

- Practical Guide To Maintaining Compliance And Avoiding Penalties

- Get Expert Accountancy Support From Ls25 Accountants

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Tax compliance definition | Meeting all legal tax obligations through accurate record-keeping, timely filing, and correct payments to HMRC |

| MTD VAT mandatory | All VAT-registered businesses must keep digital records and file returns using compatible software since April 2022 |

| MTD ITSA starts 2026 | Sole traders and landlords earning over £50,000 must submit quarterly digital updates from April 2026 |

| Quarterly filing required | Income and expense summaries due by the 7th day of the month following each quarter's end |

| Penalties for non-compliance | Late filing, incorrect records, or missed payments trigger financial penalties and interest charges from HMRC |

Understanding tax compliance for UK businesses

Tax compliance means adhering to all tax laws, filing accurate returns, and making timely payments to HMRC. For UK businesses, this involves maintaining proper records, reporting income and expenses correctly, and meeting deadlines for various tax obligations including VAT, corporation tax, and self-assessment.

Legal obligations differ between business structures but share common requirements. Sole traders must report personal income through self-assessment, whilst limited companies file corporation tax returns and may need to manage PAYE for employees. Both structures face VAT registration requirements once turnover exceeds £90,000, though voluntary registration remains available below this threshold.

Making Tax Digital fundamentally changes how businesses maintain compliance. Businesses must maintain digital accounting records and use functional compatible software to submit returns to HMRC. This shift from paper-based systems requires compatible accounting software that connects directly to HMRC systems, transforming record-keeping from optional digitalisation to mandatory digital infrastructure.

The role of tax advisors becomes increasingly valuable as compliance requirements grow more complex. Professional guidance helps businesses navigate software selection, understand quarterly filing obligations, and implement efficient record-keeping systems that satisfy HMRC requirements whilst supporting business decision-making.

Failure to comply carries serious consequences. HMRC issues penalties for late filing, charges interest on overdue payments, and can launch investigations into businesses showing persistent non-compliance. These financial penalties compound quickly, making proactive compliance far more cost-effective than reactive corrections.

Key compliance responsibilities include:

- Maintaining accurate digital records of all business transactions for at least six years

- Registering for appropriate tax schemes when income thresholds are reached

- Filing returns by specified deadlines using HMRC-approved methods

- Paying tax liabilities on time to avoid interest charges

- Responding promptly to HMRC communications and queries

Making tax digital (MTD) for VAT: rules and deadlines

MTD for VAT has been mandatory for all VAT-registered UK businesses since 1 April 2022, requiring digital records and returns via compatible software. This represents the longest-running pillar of digital tax filing, providing valuable lessons for businesses preparing for Income Tax Self Assessment changes.

Every VAT-registered business must maintain digital records regardless of turnover. Previously, only businesses with taxable turnover above £85,000 faced MTD requirements, but HMRC extended this to all VAT-registered entities. Your accounting software must preserve a digital audit trail showing how figures in VAT returns connect to underlying transactions.

Digital record-keeping for VAT must cover at least six years using HMRC-compatible software. This means spreadsheets alone no longer suffice unless they connect to bridging software that links to HMRC systems. Your chosen solution must record sales, purchases, VAT charged, and VAT reclaimed in a format that HMRC systems can read and verify.

VAT returns must be submitted digitally through functional software connected to HMRC. Manual entry through the HMRC portal is no longer permitted for MTD-registered businesses. Your software automatically populates return fields from your digital records, reducing transcription errors whilst creating an auditable link between daily transactions and quarterly submissions.

Businesses failing to comply with MTD VAT face penalties and interest charges for late filing or payment. HMRC applies a points-based penalty system for late submissions, with financial penalties triggered after accumulating too many points. Late payment interest accrues daily, making prompt settlement crucial for controlling costs.

Understanding UK tax codes and VAT helps you apply correct rates to different goods and services. Standard rate (20%), reduced rate (5%), and zero rate categories each carry specific rules about when they apply. Misclassifying supplies creates compliance issues that software alone cannot prevent without proper user knowledge.

Common pitfalls to avoid:

- Using non-compatible software that cannot connect to HMRC systems

- Failing to maintain digital links between records and VAT returns

- Missing quarterly filing deadlines due to poor calendar management

- Incorrectly applying VAT rates to complex or mixed supplies

- Neglecting to reconcile VAT accounts regularly throughout each quarter

Pro tip: Regular VAT reconciliations within your software reduce errors and the risk of penalties. Monthly reviews catch discrepancies early, allowing corrections before quarter-end submissions. This proactive approach prevents the stress of last-minute fixes and reduces the likelihood of triggering HMRC enquiries.

The VAT filing errors guide provides detailed strategies for preventing common mistakes. Learning from typical errors helps you implement controls that protect compliance whilst streamlining your quarterly processes.

MTD for income tax self assessment (ITSA): upcoming changes for sole traders and landlords

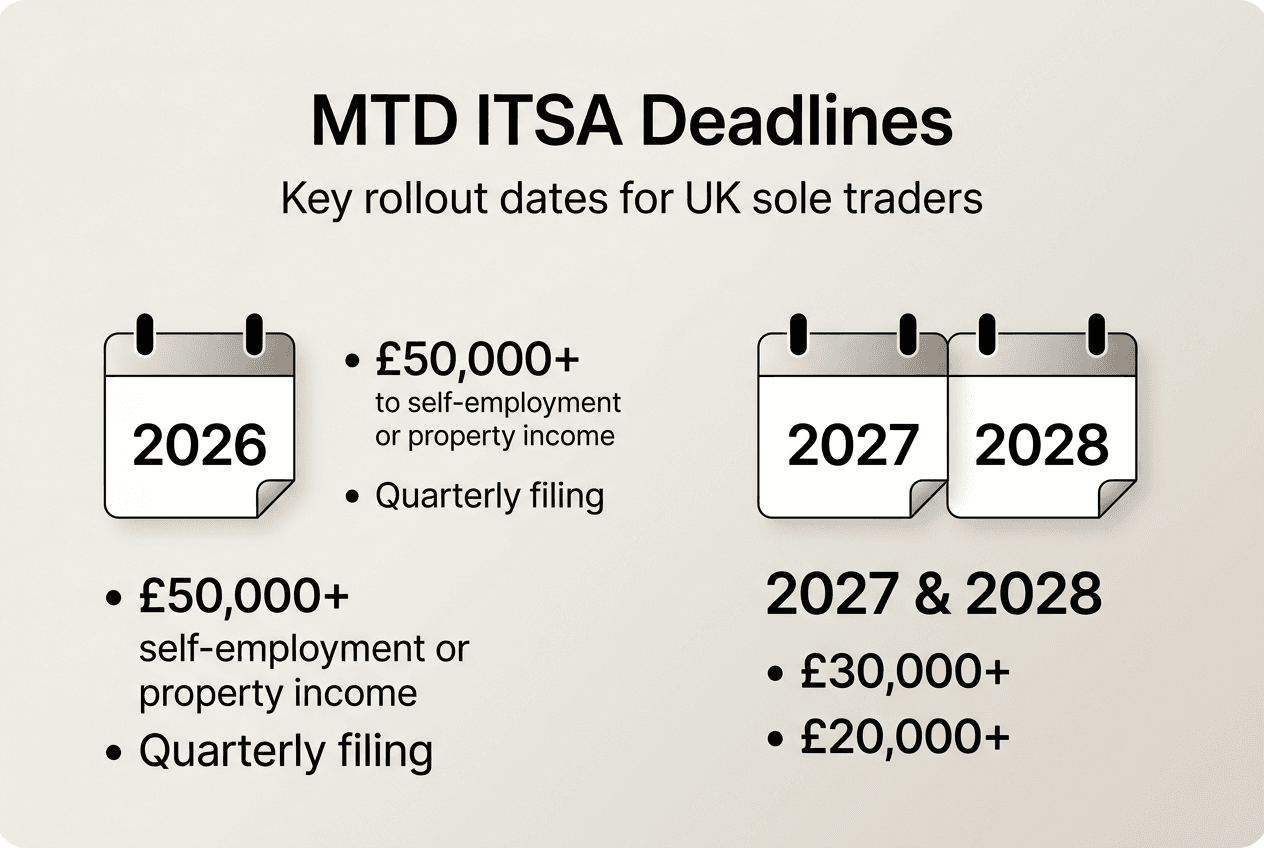

MTD for ITSA replaces annual Self Assessment tax returns for many sole traders and landlords starting April 2026. This represents the most significant change to personal tax filing in decades, shifting from annual retrospective reporting to quarterly prospective updates that mirror commercial accounting practices.

From 6 April 2026, sole traders and landlords with qualifying income over £50,000 must file quarterly updates via MTD ITSA. Qualifying income includes gross business profits before expenses and property rental income before allowable deductions. Multiple income sources combine when assessing whether you exceed the threshold.

The qualifying income threshold will reduce to £30,000 on 6 April 2027 and £20,000 by 6 April 2028. This phased approach extends compliance requirements progressively, eventually capturing most self-employed individuals and landlords. Planning for these changes now prevents rushed implementation later.

Quarterly updates are due by the 7th day of the month following the quarter's end. This means updates for periods ending 5 July, 5 October, 5 January, and 5 April must reach HMRC by 7 August, 7 November, 7 February, and 7 May respectively. These interim submissions summarise income and expenses but do not calculate final tax liabilities.

Steps to comply with MTD ITSA:

- Register for MTD ITSA through your HMRC online account before your first quarterly deadline

- Select compatible software from HMRC's approved supplier list that suits your business needs

- Maintain digital records of all business income and allowable expenses throughout each quarter

- Submit quarterly updates summarising income and expenses by the specified deadlines

- Finalise your annual return by 31 January following the tax year, declaring final tax liability

The transition from annual to quarterly reporting fundamentally changes tax administration:

| Aspect | Old Self Assessment | New MTD ITSA |

|---|---|---|

| Reporting frequency | Annual return only | Quarterly updates plus annual finalisation |

| Submission deadline | 31 January following tax year | 7th of month after each quarter |

| Record format | Paper or digital acceptable | Digital records mandatory |

| Software requirement | Optional | HMRC-compatible software required |

| Penalty structure | Single late filing penalty | Points-based system for missed quarters |

Pro tip: Early MTD ITSA adoption can simplify record management and improve cash flow forecasting. Quarterly reviews encourage regular attention to business finances, helping you spot trends, manage expenses, and prepare for tax payments rather than facing surprises at year end. This discipline often reveals opportunities to optimise tax deductions throughout the year.

The annual finalisation replaces your traditional Self Assessment return but occurs after quarterly updates. You review the year's figures, make any adjustments for items not included in quarterly submissions, and declare your final tax liability. This separation between regular reporting and final settlement mirrors how limited companies handle corporation tax.

Exemptions apply to specific groups including those earning below thresholds, partnerships (which follow separate MTD rules), and individuals with complex tax affairs requiring specialist treatment. HMRC guidance clarifies eligibility, but most sole traders and landlords should prepare for quarterly digital filing.

Practical guide to maintaining compliance and avoiding penalties

Maintaining tax compliance requires systematic processes, appropriate technology, and regular attention to deadlines. The shift to digital filing makes software selection and record-keeping practices critical success factors for UK businesses navigating MTD requirements.

Critical steps to ensure compliance:

- Register with HMRC for relevant tax schemes before reaching mandatory thresholds or starting business activities

- Choose HMRC-compatible accounting software that matches your business complexity and technical comfort level

- Keep up-to-date digital records by entering transactions promptly rather than batching them quarterly

- Submit returns timely by setting calendar reminders well before deadlines to allow for technical issues

- Reconcile accounts monthly to catch errors early and maintain confidence in your financial position

Selecting appropriate software determines how smoothly you manage compliance. Popular MTD-compatible options serve different business needs:

| Software | Best For | Key Features | Monthly Cost |

|---|---|---|---|

| Xero | Growing businesses | Bank feeds, invoicing, inventory, multi-user access | £12-£37.50 |

| QuickBooks | Established SMEs | Comprehensive reporting, payroll integration, project tracking | £10-£35 |

| FreeAgent | Freelancers | Simple interface, expense tracking, tax estimates | £19-£29 |

| Sage | Traditional firms | Desktop or cloud options, strong VAT features, established support | £10-£32 |

Common penalties under MTD include financial charges for late filing, late payment, and inadequate record-keeping. The points-based system for late submissions accumulates points for each missed deadline, with financial penalties triggered after reaching threshold levels. Late payment interest accrues daily at HMRC's published rate, currently 7.75% annually, making prompt settlement financially prudent.

Businesses must use functional compatible software to file returns and maintain digital records; failure leads to penalties. HMRC defines "functional compatible software" as products that maintain digital records, preserve audit trails, and connect directly to HMRC systems without manual intervention. Spreadsheets require bridging software to meet this standard.

Pro tip: Regularly back up digital records and reconcile accounts monthly to detect issues early. Cloud-based software typically handles backups automatically, but verifying backup integrity protects against data loss. Monthly reconciliation catches bank feed errors, duplicate entries, or miscategorised transactions before they compound into significant discrepancies.

Using compliant software transforms tax compliance from a burden into a business advantage. Real-time financial visibility supports better decisions, whilst automated filing reduces administrative time and stress. The initial investment in proper systems pays dividends through improved financial control and reduced penalty risk.

The small business accounting tips guide explores broader financial management strategies beyond basic compliance. Effective accounting integrates tax obligations with operational management, creating systems that serve multiple business purposes simultaneously.

Preventing penalties requires understanding HMRC's enforcement approach. The tax authority uses data analytics to identify non-compliance patterns, making consistent accurate filing more important than ever. Businesses showing regular late submissions or significant errors face increased scrutiny, potentially triggering compliance checks or formal investigations.

Get expert accountancy support from LS25 Accountants

Navigating tax compliance and Making Tax Digital requirements can feel overwhelming, especially when balancing business operations with evolving regulatory demands. Professional support transforms compliance from a source of stress into a managed process that protects your business whilst optimising tax efficiency.

LS25 Accountants specialises in advisory and compliance services for UK businesses of all sizes, from sole traders to established limited companies. Our team provides expert assistance on Making Tax Digital implementation, VAT compliance, Income Tax Self Assessment preparation, and strategic tax planning that aligns with your business goals.

Access practical guides and tailored accounting solutions designed specifically for businesses across the LS25 area and beyond. We offer proactive support for digital tax compliance, helping you select appropriate software, establish efficient record-keeping systems, and meet all filing deadlines confidently.

Partner with professional accountancy services to reduce errors, meet deadlines, and optimise your tax affairs. Our approach combines technical expertise with practical business understanding, ensuring compliance requirements support rather than hinder your commercial success.

Frequently asked questions

What does tax compliance mean for my UK business?

Tax compliance means meeting all legal tax obligations including accurate record-keeping, timely filing of returns, and prompt payment of liabilities to HMRC. Under Making Tax Digital, this now requires maintaining digital records using compatible software and submitting returns electronically through systems that connect directly to HMRC.

Who must comply with MTD for income tax self assessment starting 2026?

Sole traders and landlords with qualifying income over £50,000 must comply from 6 April 2026. Qualifying income includes gross business profits and rental income before expenses. The threshold reduces to £30,000 in April 2027 and £20,000 in April 2028, progressively extending requirements to smaller businesses.

What records must I keep under making tax digital?

You must maintain digital accounting records of all income, expenses, and VAT transactions using HMRC-recognised software. These records must preserve an audit trail showing how figures in your returns connect to underlying transactions. All records must be kept for at least six years and remain accessible for HMRC inspection.

What happens if I miss MTD deadlines?

HMRC imposes penalties through a points-based system for late submissions, with financial penalties triggered after accumulating multiple points. Late payment attracts daily interest charges at HMRC's published rate. Persistent non-compliance can lead to formal investigations, additional penalties, and potential legal action in severe cases.

How can I prepare for MTD ITSA changes effectively?

Register early through your HMRC online account, select compatible software from approved suppliers, and begin maintaining digital records immediately. Consider consulting a tax advisor to understand audit processes and ensure your systems meet all requirements. Practice quarterly reporting before mandatory deadlines to identify and resolve issues whilst voluntary compliance remains an option.