Most business owners assume HMRC tax audits happen randomly, catching unlucky firms off guard. That's not quite true. HMRC employs sophisticated data-driven digital systems to flag audit risks, targeting businesses based on specific triggers rather than chance. This guide explains what HMRC tax audits involve, how audits are selected, the most common triggers, and practical steps you can take to prepare effectively and minimise risk in 2026.

Table of Contents

- Introduction To HMRC Tax Audits

- Understanding How HMRC Identifies Audit Risks

- Common Triggers That Lead To HMRC Audits

- Types And Procedures Of HMRC Tax Audits

- Common Misconceptions About HMRC Audits

- How To Prepare For An HMRC Tax Audit

- Managing An HMRC Audit: Practical Guidance For Business Owners

- Summary And Next Steps For UK Businesses Facing HMRC Audits

- Get Expert Help With HMRC Audits From LS25 Accountants

- Frequently Asked Questions About HMRC Tax Audits

Key takeaways

| Point | Details |

|---|---|

| Audit targeting | Most audits result from data analytics detecting financial anomalies, not random selection. |

| Digital systems | HMRC's Connect platform uses 30+ data sources to identify compliance risks and flag discrepancies. |

| Common triggers | Late filings, financial inconsistencies, large cash transactions, and unusual dividend patterns raise red flags. |

| Record keeping | Maintaining accurate digital records and meeting Making Tax Digital requirements significantly reduce audit exposure. |

| Audit types | HMRC conducts routine checks, detailed enquiries, and criminal investigations depending on risk severity. |

Introduction to HMRC tax audits

An HMRC tax audit is a formal review where HMRC examines your business records to verify tax compliance and accuracy. Audits range from simple compliance checks to detailed enquiries and, in serious cases, criminal investigations. The purpose is straightforward: ensure businesses pay the correct amount of tax and identify errors, omissions, or deliberate evasion.

In 2026, HMRC relies heavily on digital intelligence to select audit candidates. The Connect system cross references financial data from multiple sources, including bank records, Companies House filings, property transactions, social media, and online marketplaces. Digital red flags like repeated late VAT submissions, unexplained dividend payments, and mismatches between reported income and spending patterns trigger automated alerts.

Understanding this data driven approach helps you recognise audit risks before HMRC does. Rather than fearing audits as random misfortune, view them as a compliance checkpoint where accurate records and professional guidance make all the difference. UK business owners concerned about tax compliance should treat audit readiness as an ongoing practice, not a crisis response. For comprehensive support, explore our accountancy guides tailored for LS25 businesses.

HMRC audit types include:

- Compliance checks: brief reviews of specific tax returns or records

- Full enquiries: detailed examinations of accounts, often spanning multiple tax years

- Criminal investigations: serious cases involving suspected fraud or deliberate tax evasion

Each type carries different implications for your business, from minor adjustments to significant penalties and legal consequences.

Understanding how HMRC identifies audit risks

HMRC's Connect system represents a significant shift in how tax compliance is monitored. This digital platform aggregates data from over 30 sources, creating detailed financial profiles for every UK taxpayer and business. Connect compares your reported figures against benchmarks for similar businesses, flagging outliers and inconsistencies automatically.

Benchmarking works by analysing industry norms. If your restaurant reports significantly lower turnover than comparable businesses in your area, Connect flags this discrepancy. Similarly, if your profit margins deviate sharply from sector averages without clear explanation, HMRC's algorithms prioritise your business for review.

Anomalies detected by Connect include:

- Sudden drops or spikes in reported income without corresponding business changes

- Discrepancies between VAT returns and corporation tax filings

- Lifestyle indicators that don't match declared income, such as property purchases or luxury assets

- Repeated late submissions or amendments to previously filed returns

- Gaps between Companies House accounts and HMRC tax returns

Pro Tip: Conduct quarterly reconciliations between your accounting software, bank statements, and tax submissions. Regular cross checks help you spot errors before HMRC does, reducing the likelihood of triggering audit flags.

HMRC also monitors social media and online platforms. If you advertise services on Facebook but declare minimal income, or purchase high value assets whilst reporting losses, these contradictions raise immediate red flags. The key is consistency. Your financial records should tell a coherent story across all platforms and submissions. For detailed guidance on maintaining compliant records, visit our accountancy resources.

Common triggers that lead to HMRC audits

Certain behaviours and circumstances consistently attract HMRC attention. Understanding these triggers allows you to identify and correct risks proactively, reducing your audit exposure.

Late or incorrect tax submissions rank among the most frequent audit triggers. Missing deadlines, submitting incomplete returns, or repeatedly amending filed documents signals poor financial management and raises questions about accuracy. HMRC interprets persistent late filings as a compliance risk indicator, prompting closer scrutiny.

Financial inconsistencies between different tax filings create immediate red flags. For example, reporting high turnover on VAT returns but low profits on corporation tax returns suggests either errors or deliberate underreporting. Similarly, large dividend payments from companies with minimal profits attract attention, as HMRC questions how such distributions are justified.

Cash based businesses face higher audit risk because transactions are harder to trace and record keeping often contains errors. Restaurants, trades, hairdressers, and similar sectors experience disproportionate HMRC scrutiny due to cash handling vulnerabilities.

"Cash based businesses such as restaurants and trades show higher audit risk due to less traceable transactions and bookkeeping errors. HMRC prioritises these sectors for compliance checks."

Other common triggers include:

- Declaring consistent losses over multiple years without credible business plans or corrective action

- Lifestyle expenditures that exceed declared income, flagged through property purchases, vehicle registrations, or overseas travel

- Round number expenses that appear estimated rather than documented with receipts

- Frequent changes in accounting methods or business structure without clear commercial reasons

For practical advice on managing cash flow and reducing audit risks, see our guide on managing business cash flow.

Types and procedures of HMRC tax audits

HMRC employs different audit approaches depending on perceived risk and complexity. Understanding what each involves helps you prepare appropriately and respond effectively.

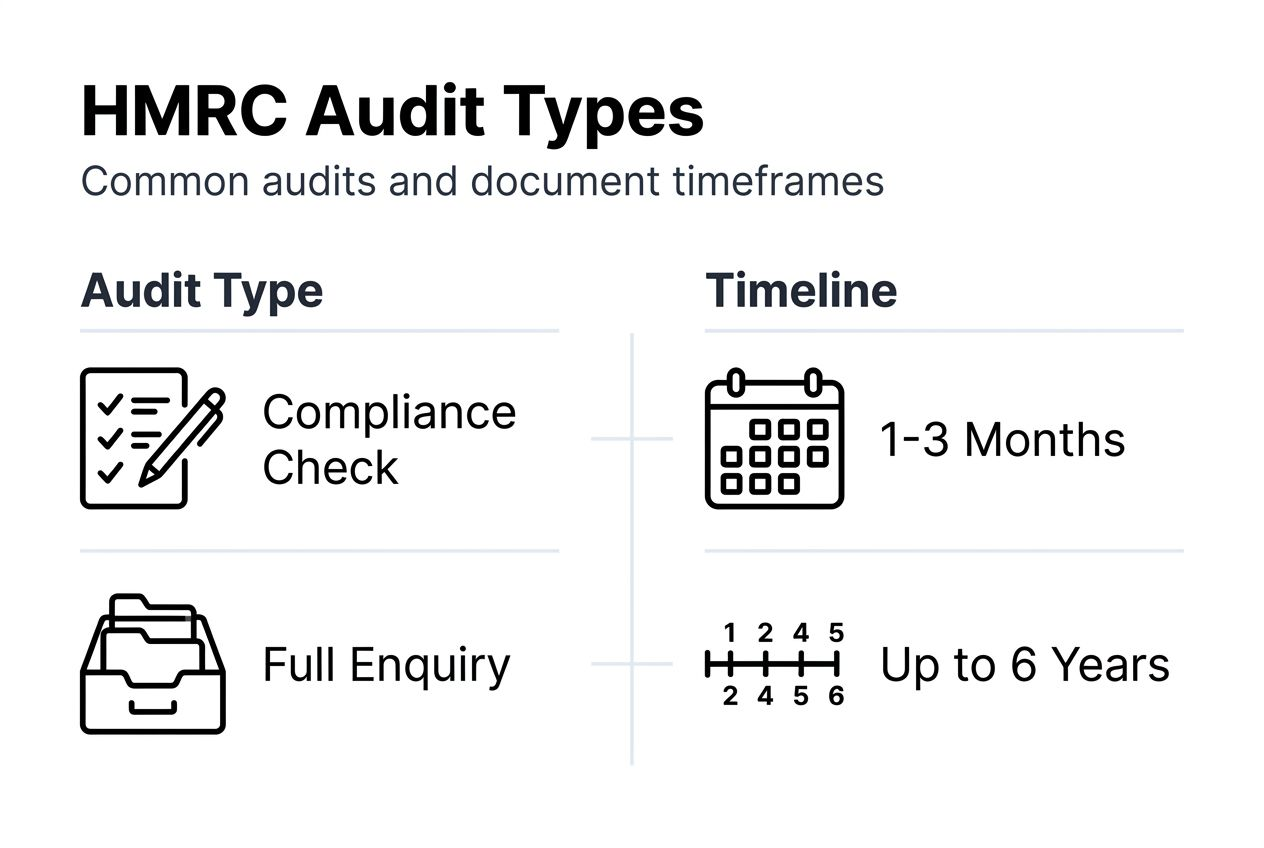

| Audit Type | Scope | Duration | Typical Outcome |

|---|---|---|---|

| Compliance check | Specific return or claim | 1-3 months | Minor adjustments or no change |

| Full enquiry | Complete accounts, multiple years | 6-18 months | Significant adjustments, penalties possible |

| Criminal investigation | Suspected fraud | 12+ months | Prosecution, substantial penalties |

Routine compliance checks verify specific details or claims, such as expense deductions or VAT reclaims. HMRC typically requests supporting documents and resolves these reviews within weeks. Full enquiries dig deeper, examining entire accounting periods and cross referencing multiple data sources. Criminal investigations are reserved for cases where HMRC suspects deliberate fraud, involving formal interviews under caution and potential prosecution.

Typical audit procedures follow these steps:

- Initial contact: HMRC sends a formal notice explaining the review scope and requesting specific documents

- Document submission: You provide requested records, including invoices, bank statements, contracts, and accounting files

- Clarification: HMRC may request additional information or explanations for specific transactions

- Site visit: For detailed enquiries, HMRC officers may visit your premises to inspect records and interview staff

- Findings: HMRC issues a report outlining discrepancies, proposed adjustments, and any penalties

- Resolution: You can accept findings, negotiate adjustments, or appeal through formal channels

HMRC can investigate up to six years of past records in routine cases, extending to 20 years for serious fraud. Documents commonly requested include sales invoices, purchase receipts, payroll records, bank statements, VAT returns, and contracts with suppliers or clients.

Professional representation becomes crucial during full enquiries and investigations. Tax advisors understand HMRC procedures, protect your legal rights, and negotiate favourable outcomes. Learn more about the benefits of hiring a tax advisor to guide you through complex audits.

Common misconceptions about HMRC audits

Many business owners hold inaccurate beliefs about HMRC audits that create unnecessary anxiety or lead to poor responses. Correcting these misconceptions helps you approach audits rationally and strategically.

Myth: HMRC audits are random. Reality: Most audits result from data analytics identifying specific risk patterns, not random selection. Connect algorithms prioritise businesses showing compliance red flags, making audits highly targeted.

Myth: An audit means HMRC suspects fraud. Reality: Many audits are routine compliance checks verifying accuracy. HMRC conducts thousands of reviews annually as standard procedure, and being selected doesn't imply wrongdoing. Errors happen, and HMRC distinguishes between innocent mistakes and deliberate evasion.

Key misconceptions to avoid:

- Believing HMRC only audits recent tax years: HMRC can review up to six years of records routinely, extending further for serious cases

- Assuming audits always result in penalties: If your records are accurate and compliant, audits often conclude with no changes or minor adjustments

- Thinking you can ignore audit notices: Failing to respond escalates investigations and increases penalty risk significantly

- Believing small businesses escape scrutiny: HMRC targets businesses of all sizes, with small firms often flagged for sector specific risks

Pro Tip: Maintain proactive communication with HMRC throughout any review. Prompt, transparent responses demonstrate good faith and often result in more favourable treatment, including reduced penalties if errors are discovered.

Understanding audit realities reduces fear and encourages proper preparation rather than panic.

How to prepare for an HMRC tax audit

Proactive preparation significantly reduces audit risk and minimises disruption if HMRC does initiate a review. Implementing these practices positions your business for compliance success.

Digital record keeping is non negotiable in 2026. Making Tax Digital (MTD) requires VAT registered businesses to maintain digital records and submit returns through compatible software. Beyond MTD compliance, digital systems provide audit trails that demonstrate accuracy and facilitate quick document retrieval during reviews.

Best practices for audit readiness include:

- File all tax returns accurately and on time, avoiding late submission penalties and compliance flags

- Maintain organised financial records with clear documentation for every transaction, including invoices, receipts, and bank statements

- Separate business and personal finances completely, using dedicated business accounts to prevent confusion

- Conduct regular internal reviews to identify and correct discrepancies before HMRC notices them

- Reconcile accounts monthly, ensuring consistency between bank statements, accounting software, and tax submissions

Pro Tip: Use approved digital accounting software that integrates with HMRC systems. Cloud based platforms like Xero or QuickBooks streamline compliance, reduce errors, and demonstrate professional financial management during audits.

Engage a qualified accountant or tax advisor early, ideally before problems arise. Professional support limits investigation scope and reduces personal exposure by ensuring compliance from the start. Tax advisors identify risks you might miss and implement preventative measures tailored to your business sector.

For specific guidance on reducing filing errors, explore our VAT filing error reduction guide. Regular reviews of your accounting practices can cut errors by 30 per cent, significantly lowering audit risk. Understanding the benefits of hiring a tax advisor can transform your compliance approach and deliver substantial cost savings.

Managing an HMRC audit: practical guidance for business owners

If HMRC initiates an audit, your response significantly influences the outcome. Strategic management minimises penalties, protects your business reputation, and resolves issues efficiently.

Respond promptly to all HMRC communications. Delays create suspicion and may escalate reviews into more serious investigations. Acknowledge receipt of notices immediately and provide requested documents within specified timeframes. Clear, professional communication demonstrates cooperation and good faith.

Best practices during active audits:

- Organise all requested documents systematically before submission, ensuring completeness and accuracy

- Maintain detailed records of every interaction with HMRC, including dates, names, discussion topics, and agreed actions

- Provide only what HMRC requests; volunteering additional information can expand audit scope unnecessarily

- Stay professional and courteous in all communications, avoiding defensiveness or confrontation

- Document your business processes and decision making rationale to explain transactions that might appear unusual

Early corrective action reduces audit scope substantially. If you discover errors before HMRC raises them, proactively disclose and correct them. HMRC views voluntary disclosure favourably, often reducing or eliminating penalties for genuine mistakes.

Engage professional representation when audits become complex or adversarial. Tax advisors negotiate with HMRC on your behalf, protecting your interests whilst maintaining constructive relationships. They understand technical tax law, procedural rights, and settlement options that most business owners don't. For expert support, consider hiring a tax advisor experienced in HMRC negotiations.

If HMRC proposes adjustments or penalties you disagree with, you have formal appeal rights. Professional advisors guide you through appeals processes, increasing your chances of favourable outcomes.

Summary and next steps for UK businesses facing HMRC audits

HMRC tax audits in 2026 are data driven, targeted reviews designed to verify compliance and identify tax discrepancies. Understanding how HMRC's digital systems flag risks empowers you to address vulnerabilities proactively, reducing audit likelihood and severity.

Key insights to remember:

- HMRC uses sophisticated analytics to identify audit candidates based on financial anomalies and sector specific risk factors

- Common triggers include late filings, cash heavy operations, financial inconsistencies, and lifestyle indicators that don't match declared income

- Maintaining accurate digital records and meeting Making Tax Digital requirements are fundamental to audit readiness

- Professional tax advice significantly reduces risks and improves outcomes during reviews

- Regular internal audits and reconciliations help you detect and correct errors before HMRC identifies them

Moving forward, adopt audit readiness as ongoing business practice rather than crisis response. Implement robust digital record keeping, engage professional advisors early, and monitor HMRC compliance updates regularly. Tax regulations evolve, and staying informed protects your business from unexpected exposure.

Proactive compliance isn't just about avoiding audits. It delivers operational benefits including better financial visibility, improved decision making, and reduced accounting costs through efficient processes. The businesses that thrive under HMRC scrutiny are those that treat compliance as competitive advantage, not burden.

Get expert help with HMRC audits from LS25 Accountants

Navigating HMRC audits requires expertise and experience that most business owners simply don't have time to develop. LS25 Accountants specialises in supporting UK businesses through tax compliance challenges, from audit preparation to active representation during HMRC reviews.

Our team provides tailored advice based on your specific business sector, financial situation, and compliance history. We help you organise records, implement digital accounting systems, and address risks before they trigger HMRC attention. When audits do occur, we stand beside you, managing communications and negotiating favourable outcomes.

One client recently said, "LS25 Accountants transformed our audit nightmare into a manageable process. Their expertise saved us thousands in penalties and gave us confidence we'd never felt with HMRC."

Pro Tip: Early consultation with LS25 Accountants minimises audit disruption and protects your finances. Don't wait until HMRC contacts you. Contact LS25 Accountants today to assess your compliance position and implement protective measures.

Frequently asked questions about HMRC tax audits

What are the first steps if an HMRC audit notice is received?

Acknowledge receipt immediately and review the notice carefully to understand the scope and documents requested. Contact a qualified tax advisor before responding substantively, as professional guidance from the start protects your interests and ensures proper procedure. Organise the requested documents systematically and respond within HMRC's specified timeframe.

How long does an HMRC audit usually take?

Simple compliance checks often conclude within one to three months. Full enquiries examining complete accounts typically last six to eighteen months depending on complexity and cooperation. Criminal investigations can exceed twelve months and involve formal legal procedures. Timeline depends on audit scope, document availability, and whether disputes arise requiring negotiation or appeals.

Can HMRC audit a business more than once for the same period?

Generally, HMRC won't reopen settled enquiries unless new information suggests fraud or significant errors were missed. However, different tax types can be reviewed separately, so a VAT audit doesn't prevent a later corporation tax enquiry for the same period. If HMRC discovers evidence of serious irregularities during one review, they may expand scope to cover additional periods or tax types.

What documents should be kept to satisfy an audit?

Maintain complete records for at least six years, including sales invoices, purchase receipts, bank statements, payroll records, VAT returns, contracts, and correspondence with suppliers and clients. Digital backups are essential, and documents must be readily accessible. Making Tax Digital requires digital record keeping for VAT, but good practice extends this to all business finances regardless of legal requirements.

Are there penalties if errors are found but no fraud is intended?

Yes, HMRC can impose penalties for careless errors even without fraudulent intent, though penalties are generally lower than for deliberate evasion. Penalty levels depend on error severity and whether disclosure was prompted or unprompted. Voluntary disclosure before HMRC raises issues significantly reduces penalties, often to zero for genuine mistakes corrected proactively. Reasonable care and prompt correction demonstrate good faith that HMRC considers favourably.